PythonQuant

Blackarbs Retirement Strategy Algorithm Debut (Part 1)

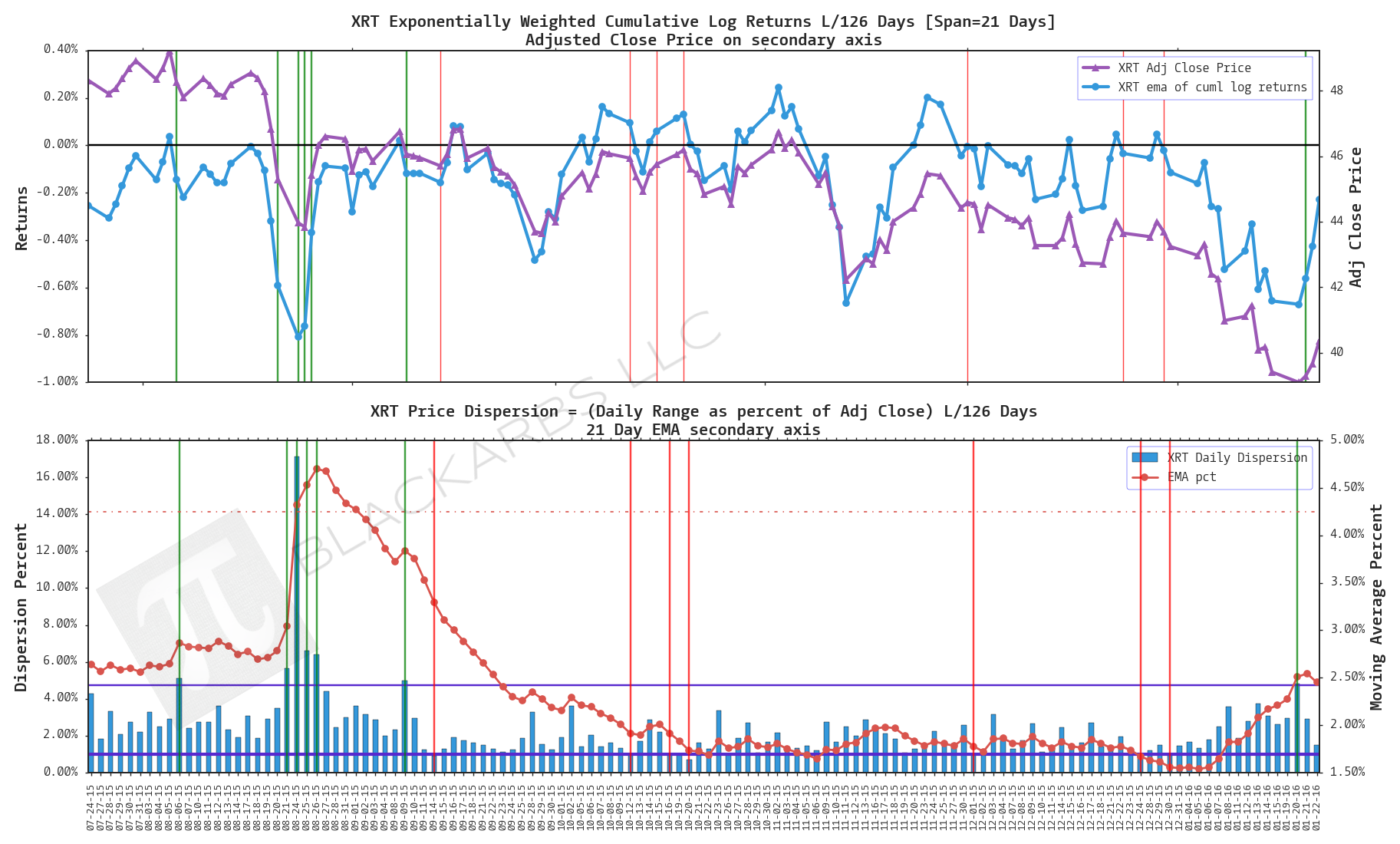

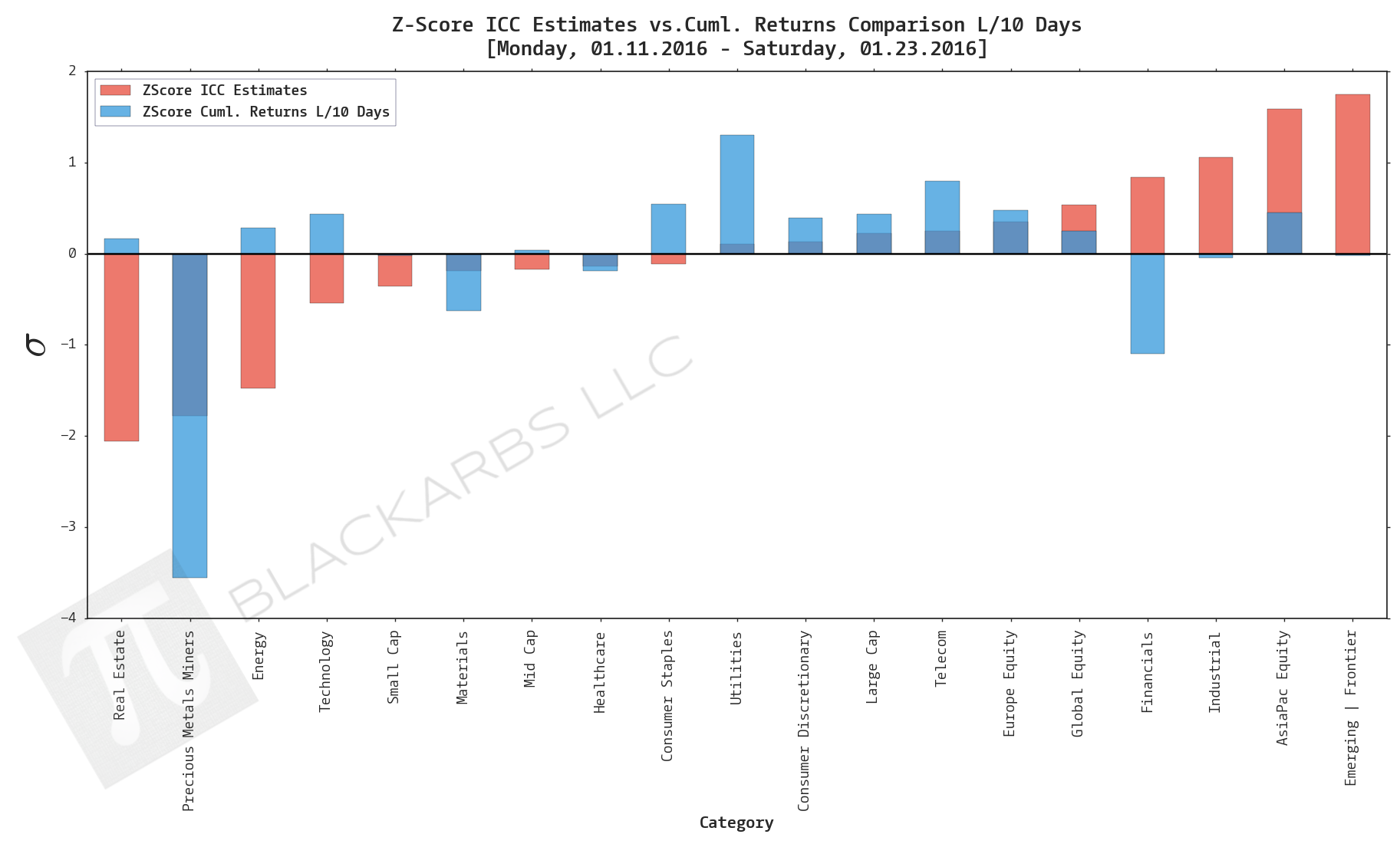

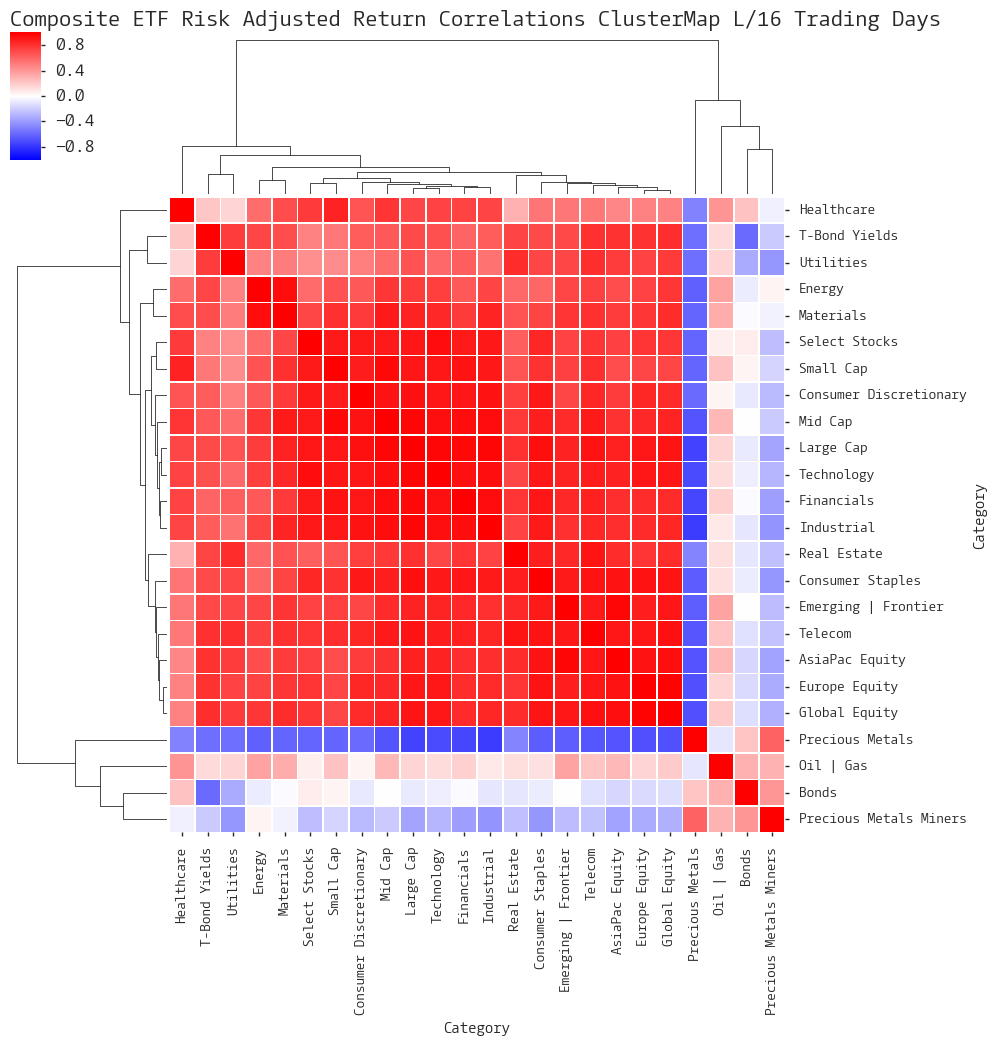

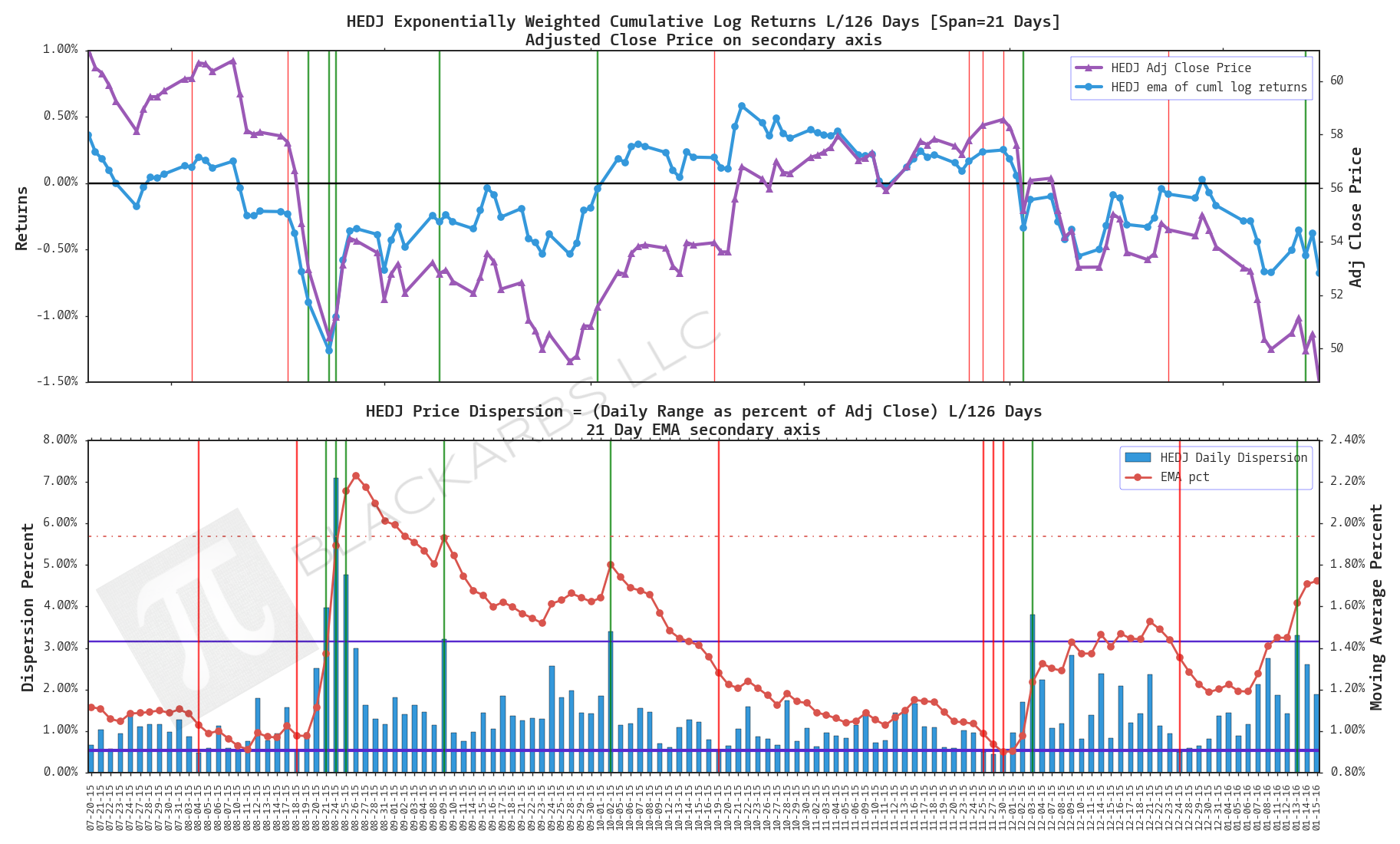

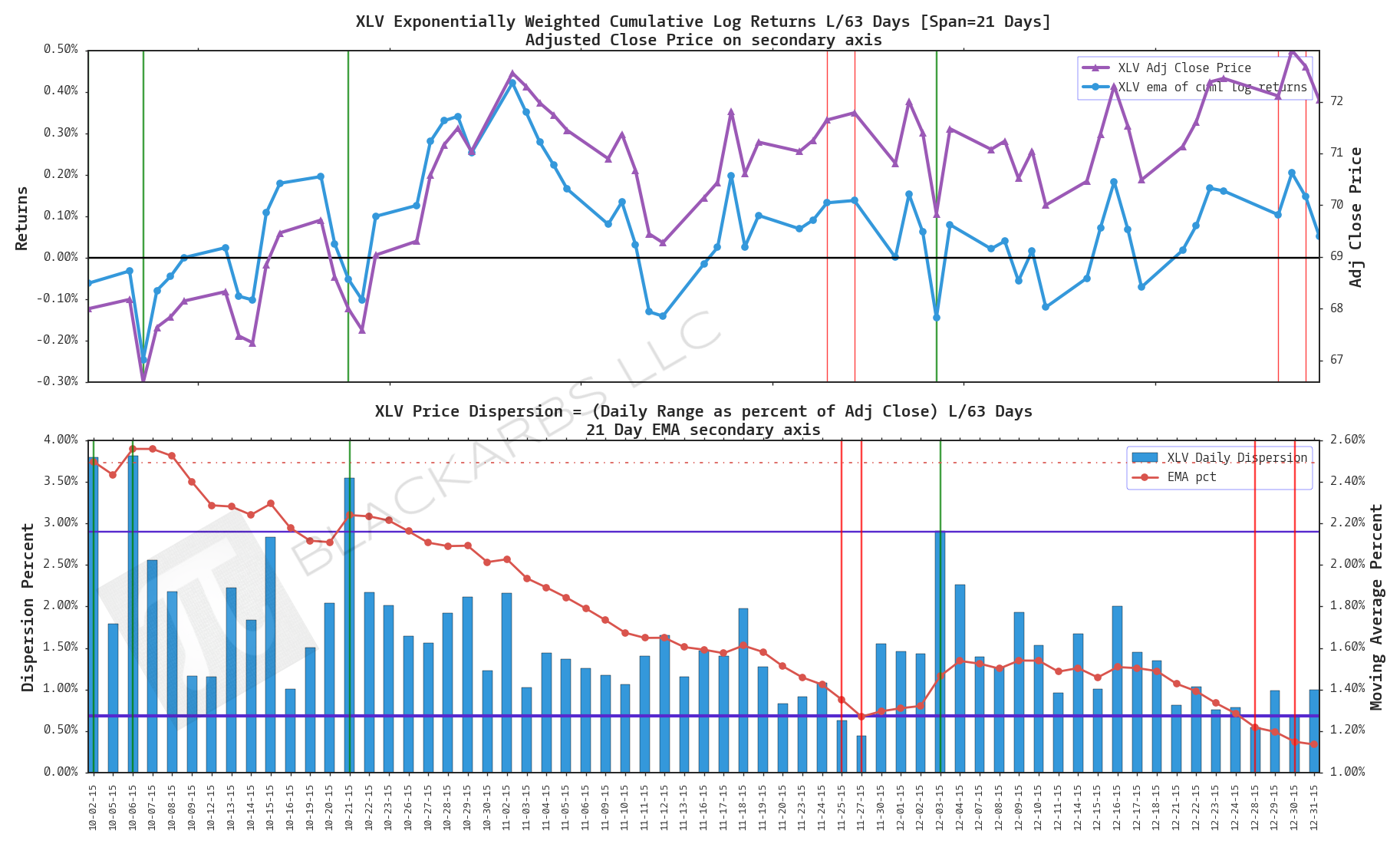

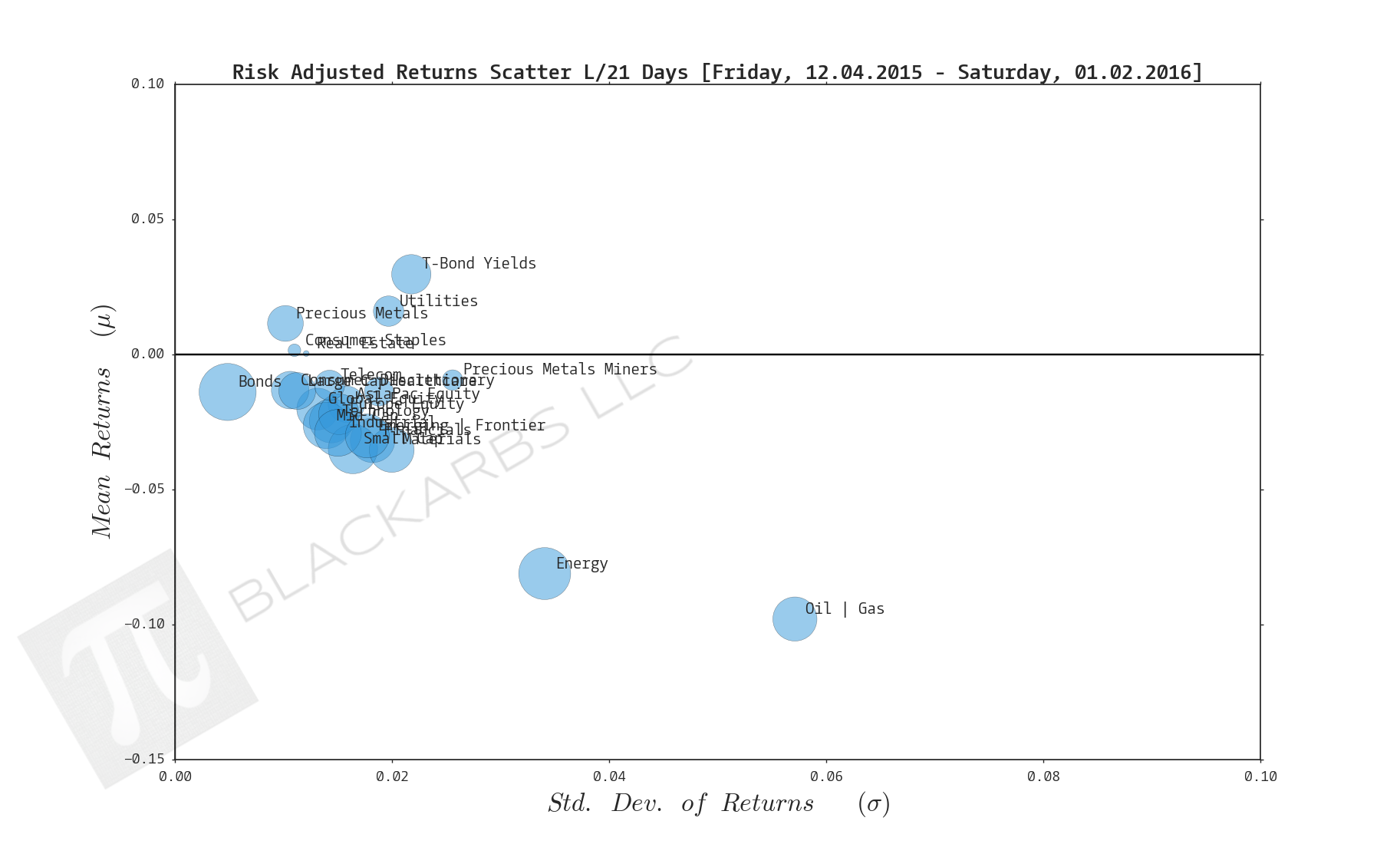

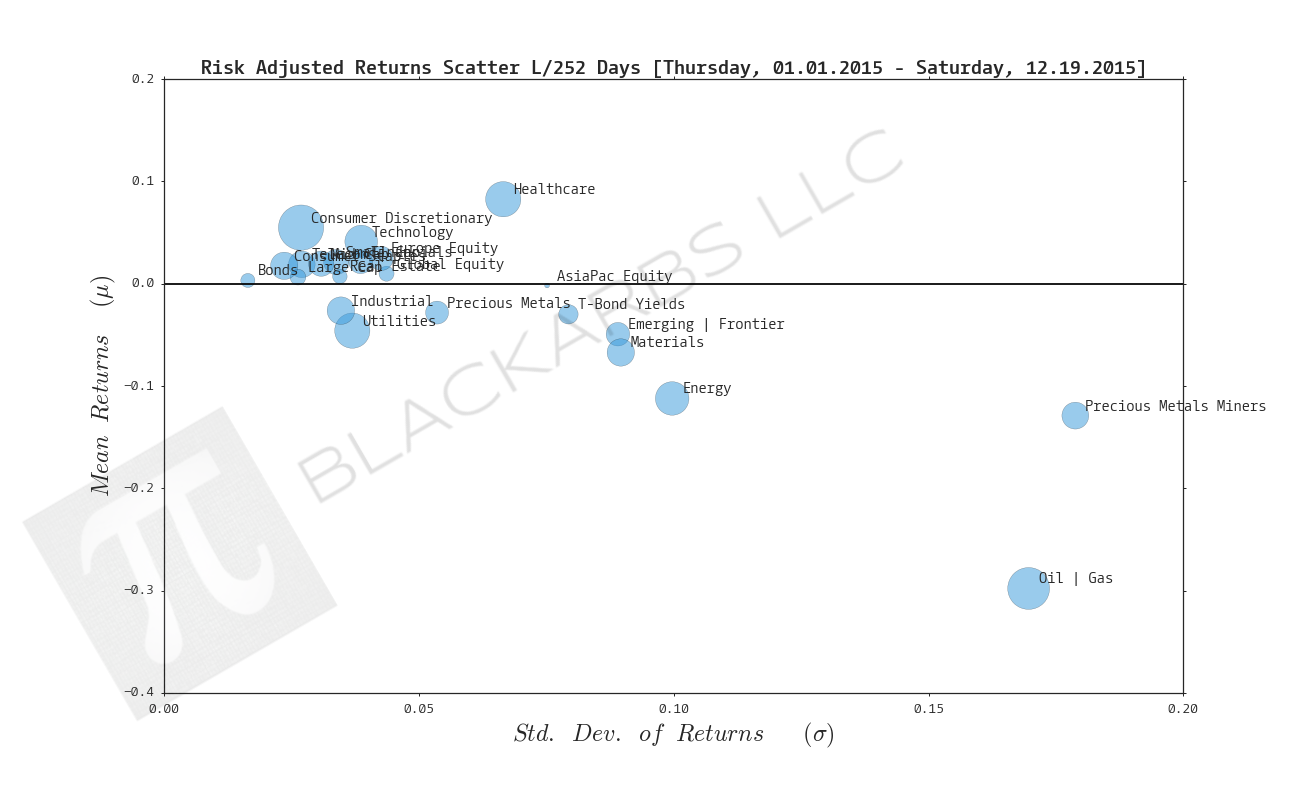

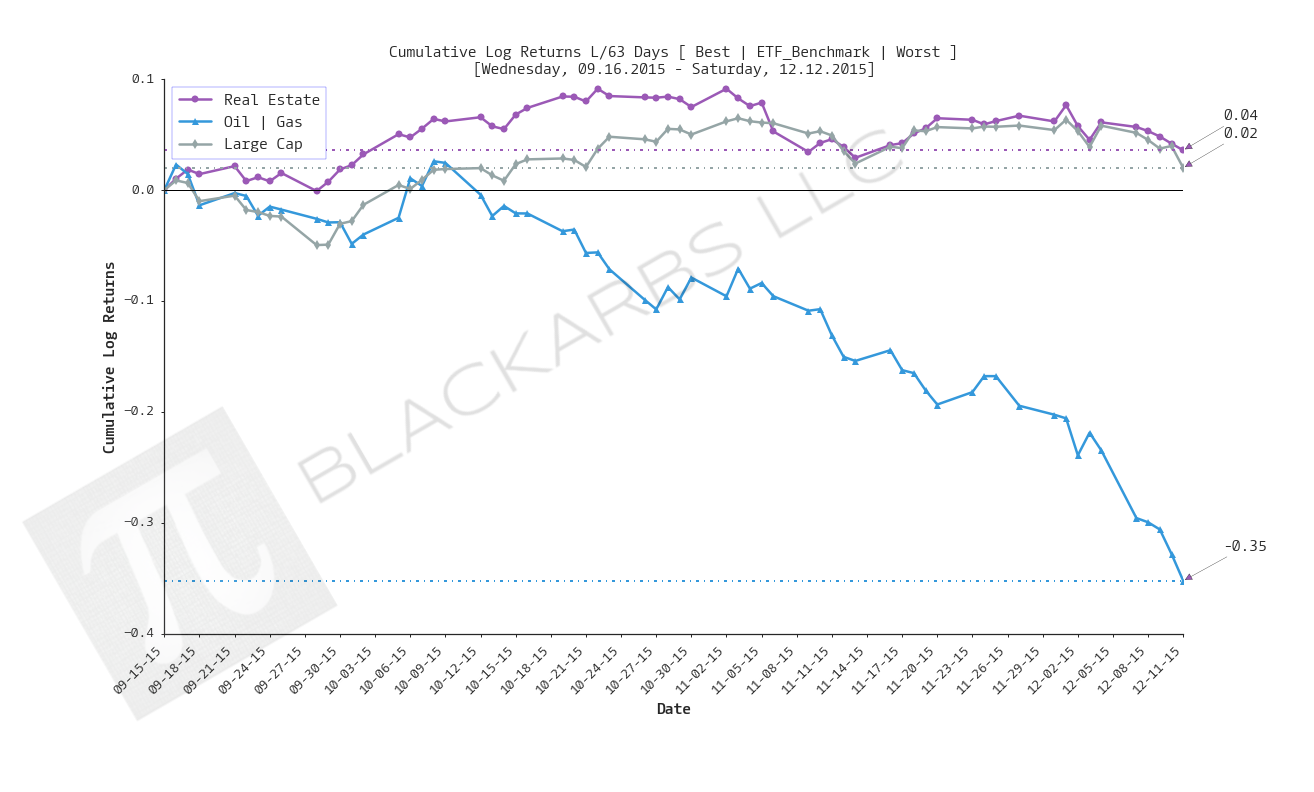

Join the growing Blackarbs Research Group Discord community here Get access to the strategy that has returned 48% in live trading since this article was written here (Updated: 2024-Mar-02) Mission Recap Blackarbs current mission is to create automated strategies with the goal of beating the market with superior risk adjusted returns. Originally, I wanted to illuminate some of the more hidden aspects of markets and investing that I found interesting and of value. Over time, that goal crystall

READ MORE →

![COMPOSITE SECTOR ETF VALUATION REPORT [7.6.2015]](https://images.squarespace-cdn.com/content/v1/53ac905ee4b003339a856a1d/1436250523268-PX9UJBTHY39NALCWY831/image-asset.png/img.png)

![Composite Sector ETF Valuation Report [6.15.2015]](https://images.squarespace-cdn.com/content/v1/53ac905ee4b003339a856a1d/1434379959959-DE9ZBLAQOS1O0KECSOWK/image-asset.png/img.png)

![COMPOSITE SECTOR ETF VALUATION UPDATED [5.24.2015]](https://images.squarespace-cdn.com/content/v1/53ac905ee4b003339a856a1d/1432487411121-MTTLFLABAOM2TUW8U3XZ/image-asset.png/img.png)

![Composite Sector ETF Valuation updated [5.10.2015]](https://images.squarespace-cdn.com/content/v1/53ac905ee4b003339a856a1d/1431314948330-G43HVEQVV34RD704GZTZ/image-asset.png/img.png)