PythonGlobal Markets

USING IMPLIED VOLATILITY TO PREDICT ETF RETURNS (2/27/16)

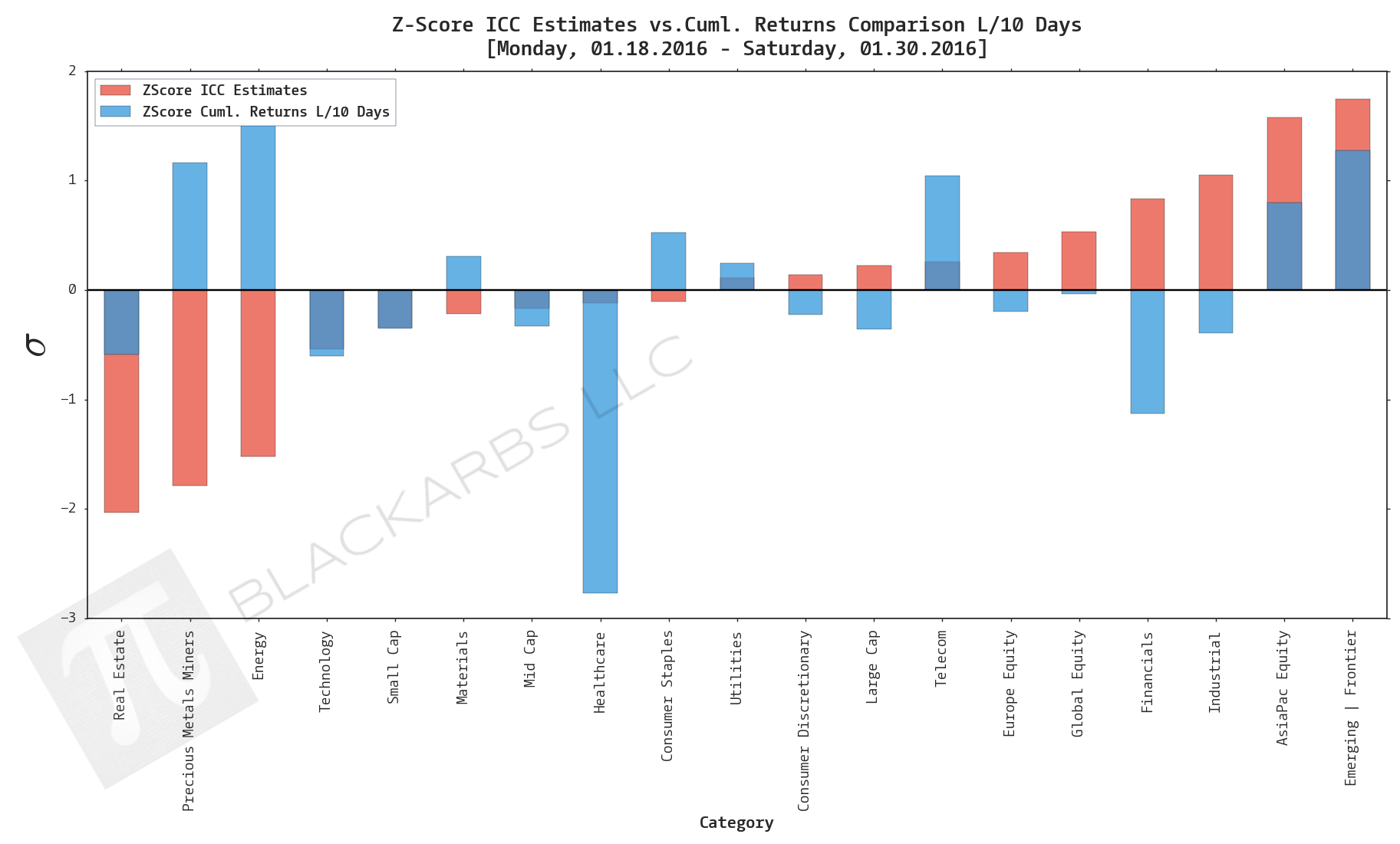

#block-yui_3_17_2_1_1456604859059_182762 .social-icons-style-border .sqs-svg-icon--wrapper { box-shadow: 0 0 0 2px inset; border: none; } FOR A DEEPER DIVE INTO ETF PERFORMANCE AND RELATIVE VALUE SUBSCRIBE TO THE ETF INTERNAL ANALYTICS PACKAGE HERE To see the origin of this series click here In the paper that inspired this series ("What Does Individual Option Volatility Smirk Tell Us About Future Equity Returns") the authors' research shows that their calculation of the Option Volatility Smi

READ MORE →