Global MarketsPython

COMPOSITE MACRO ETF WEEKLY ANALYTICS (2/13/2016)

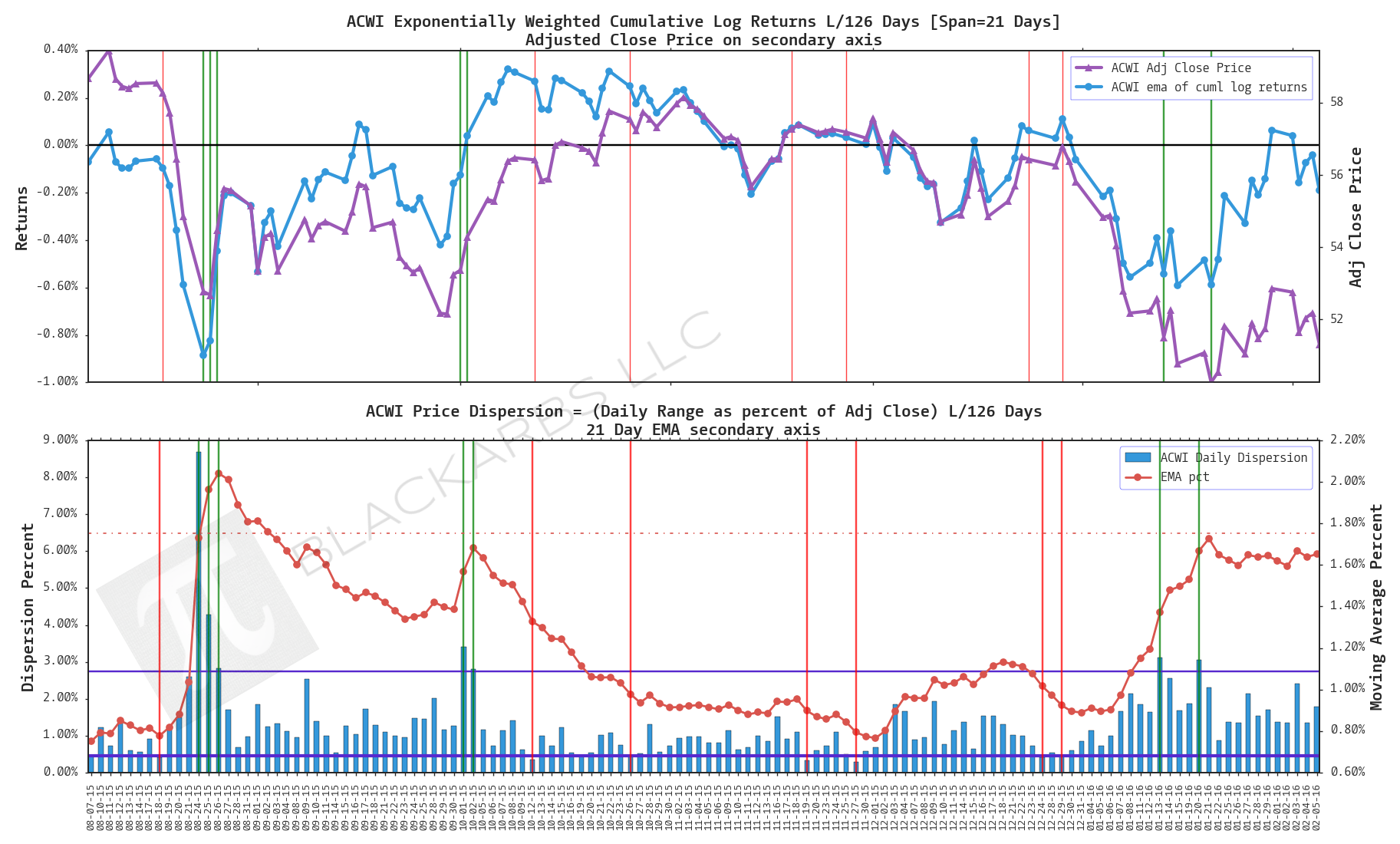

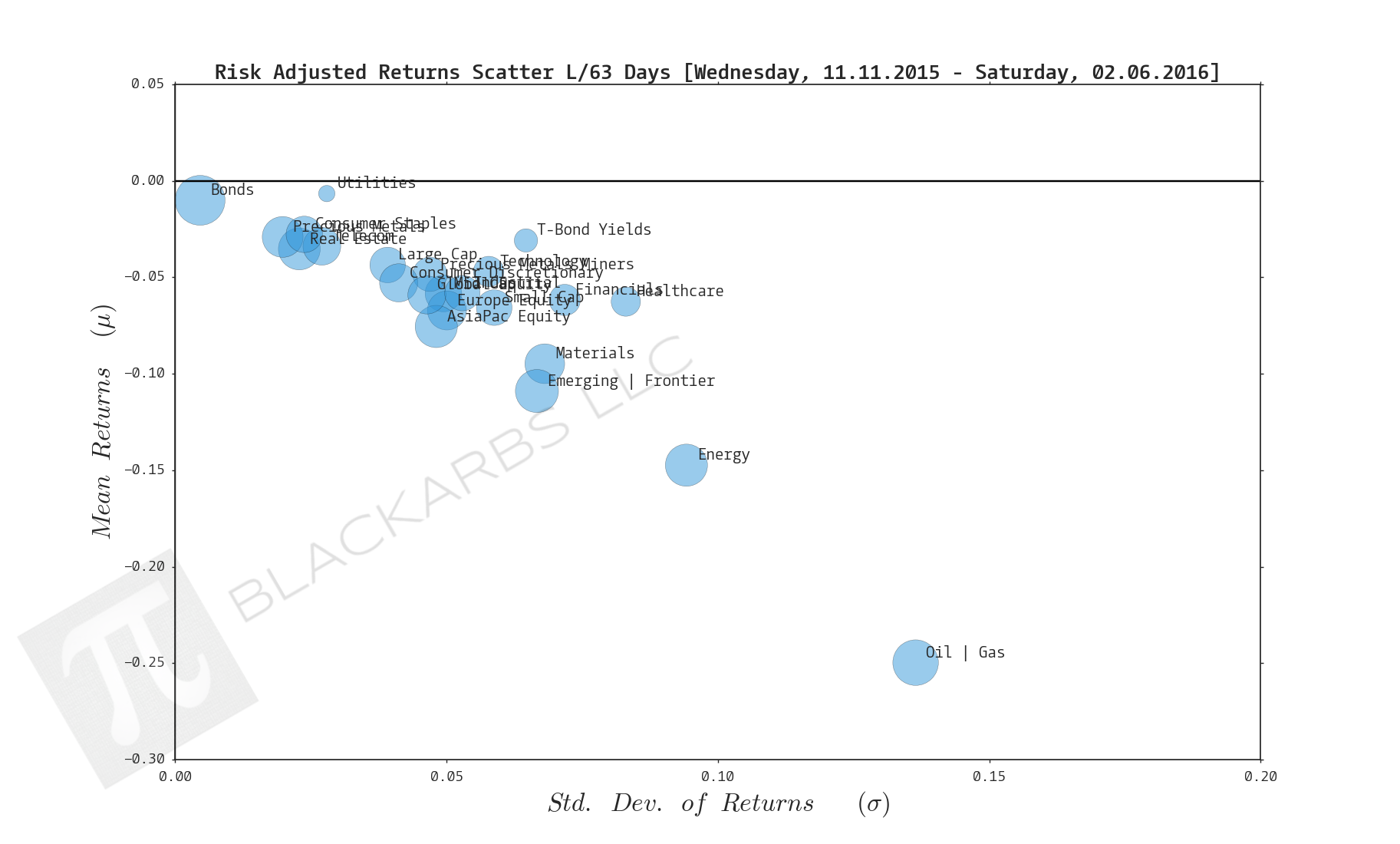

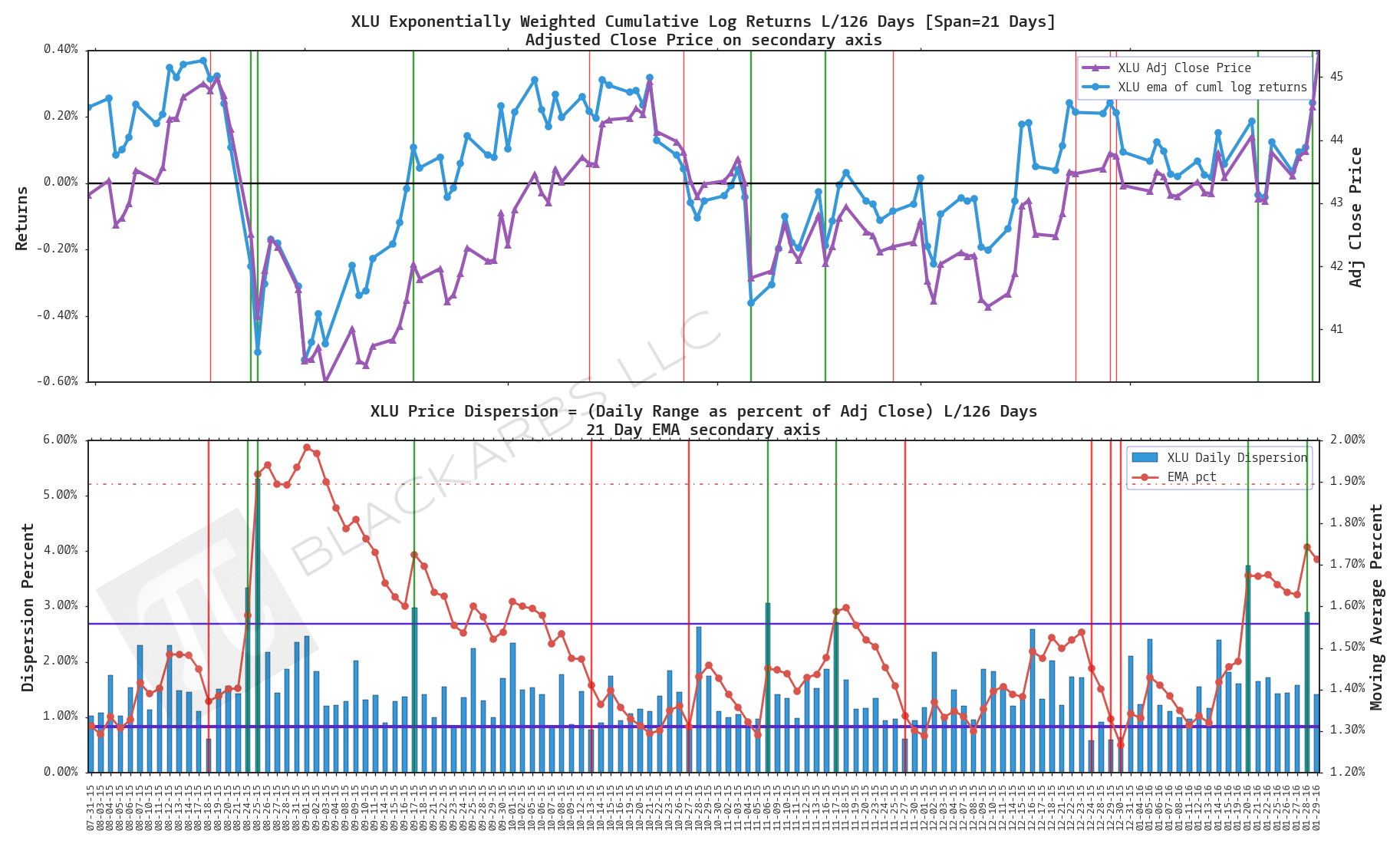

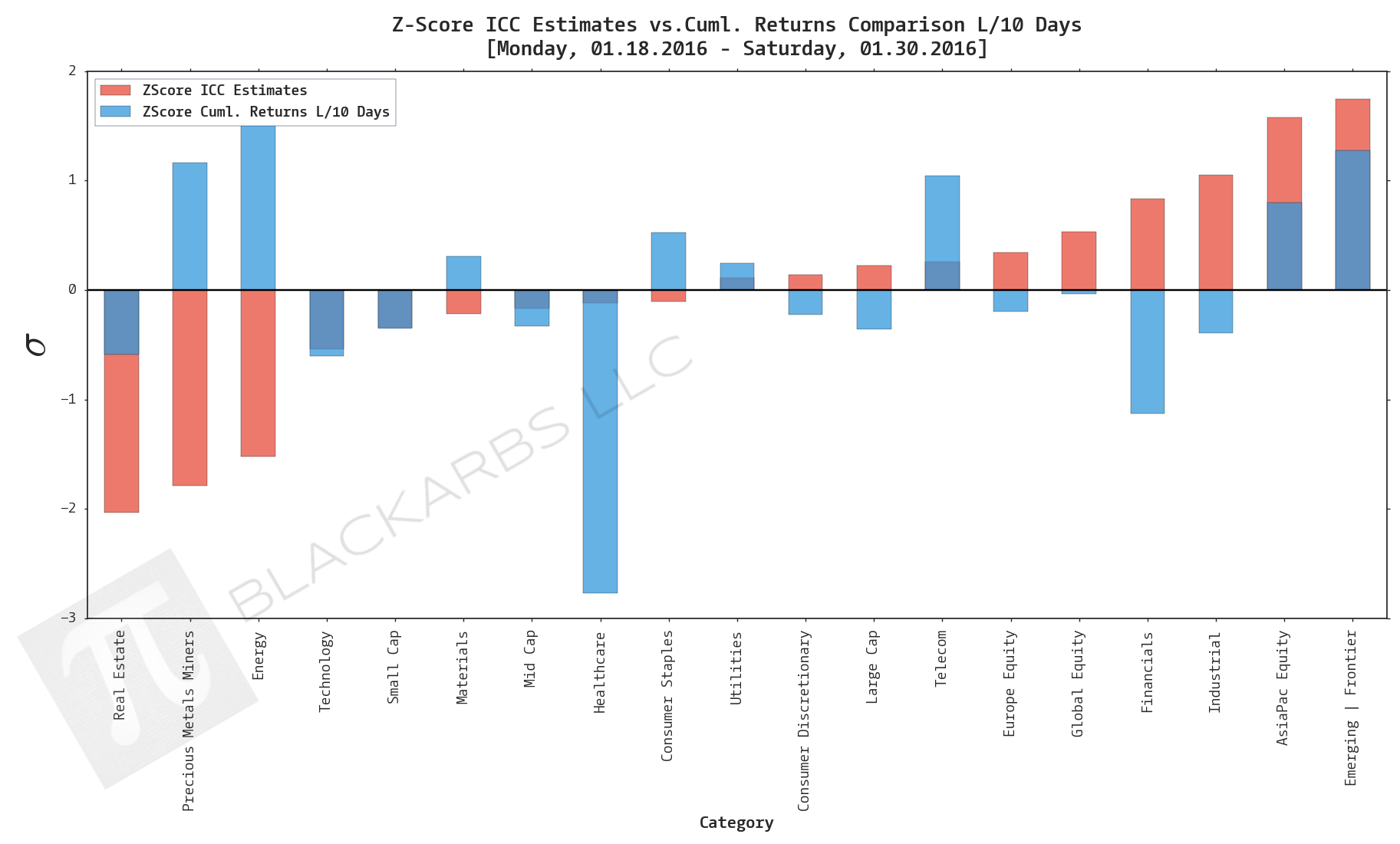

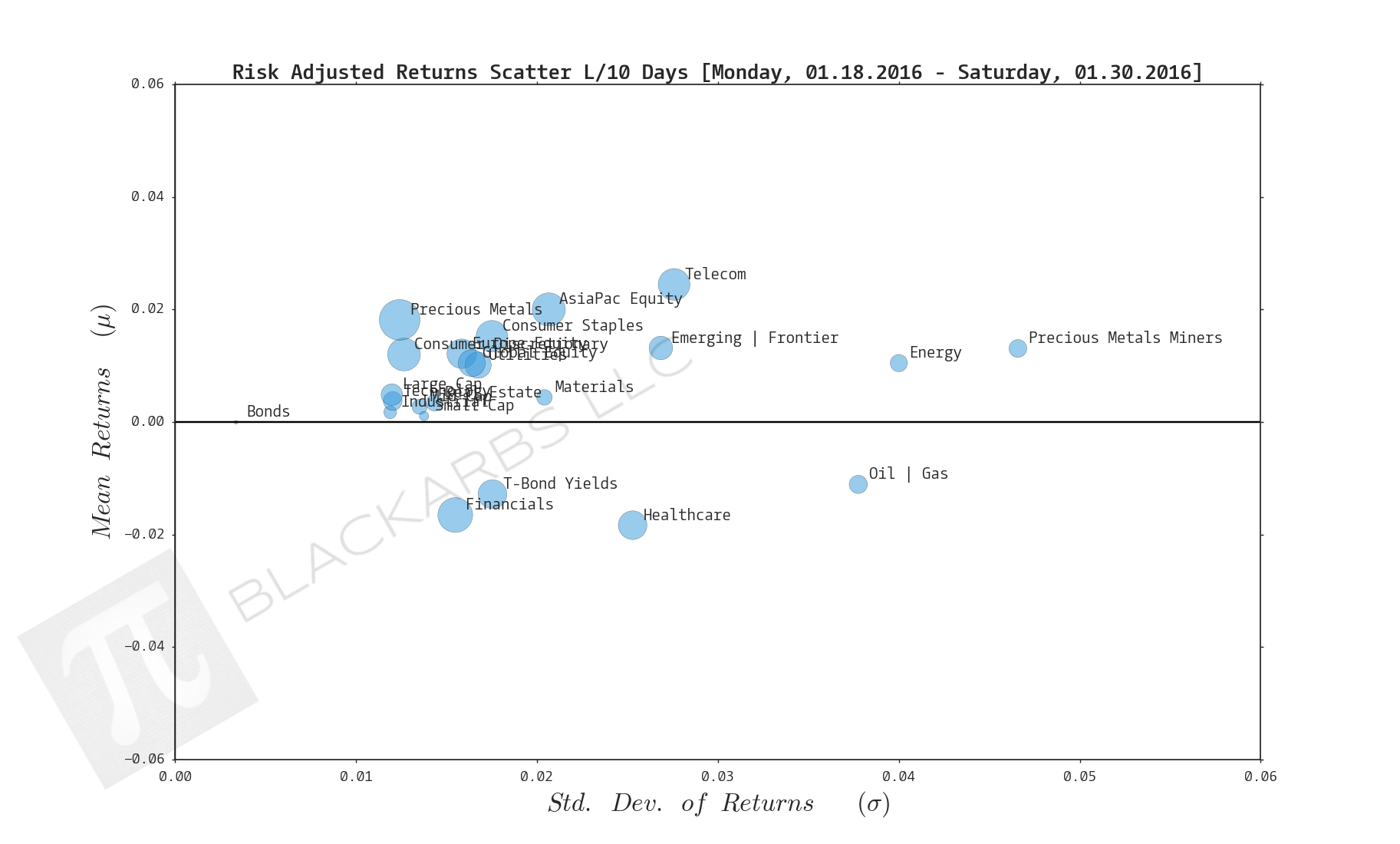

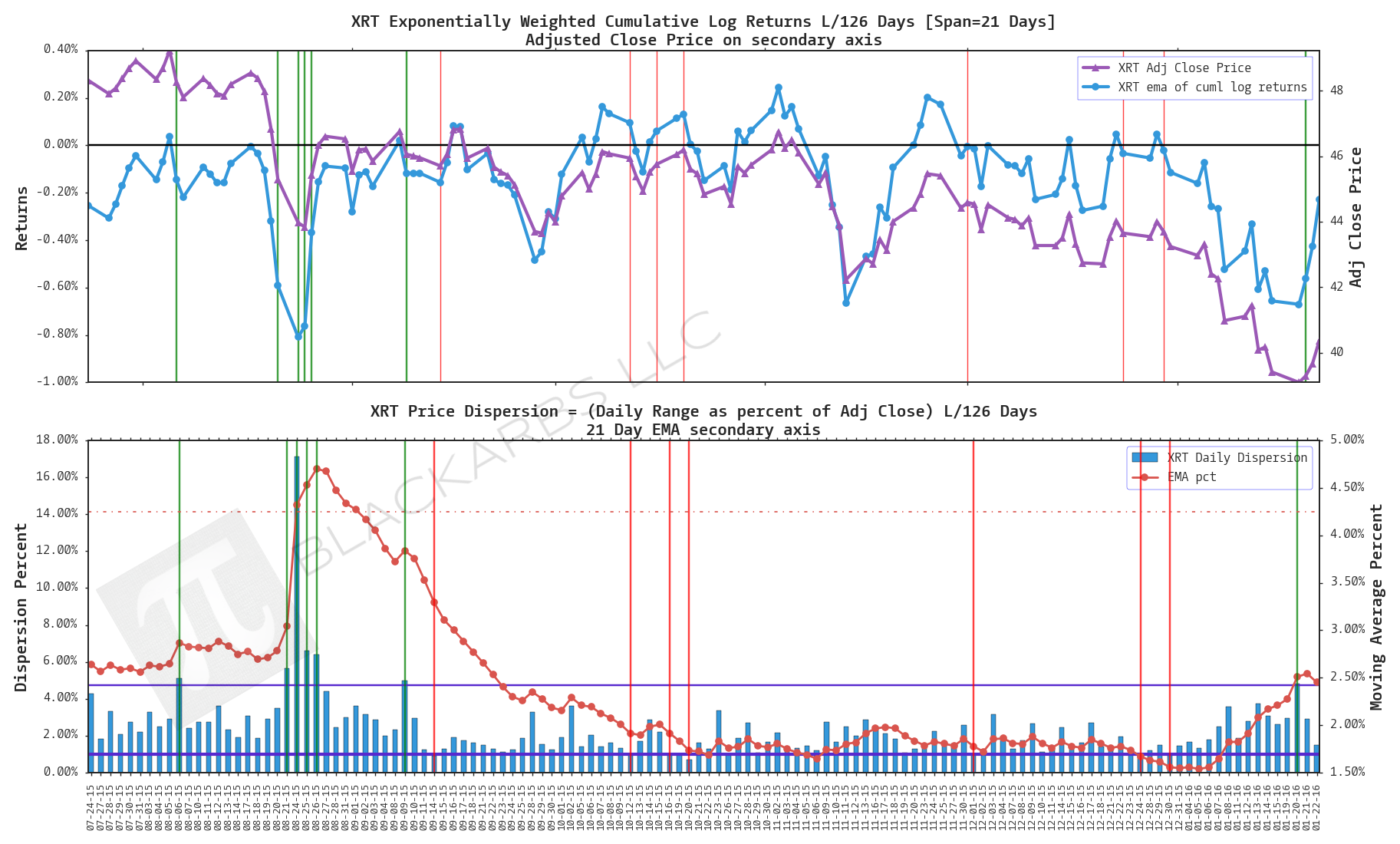

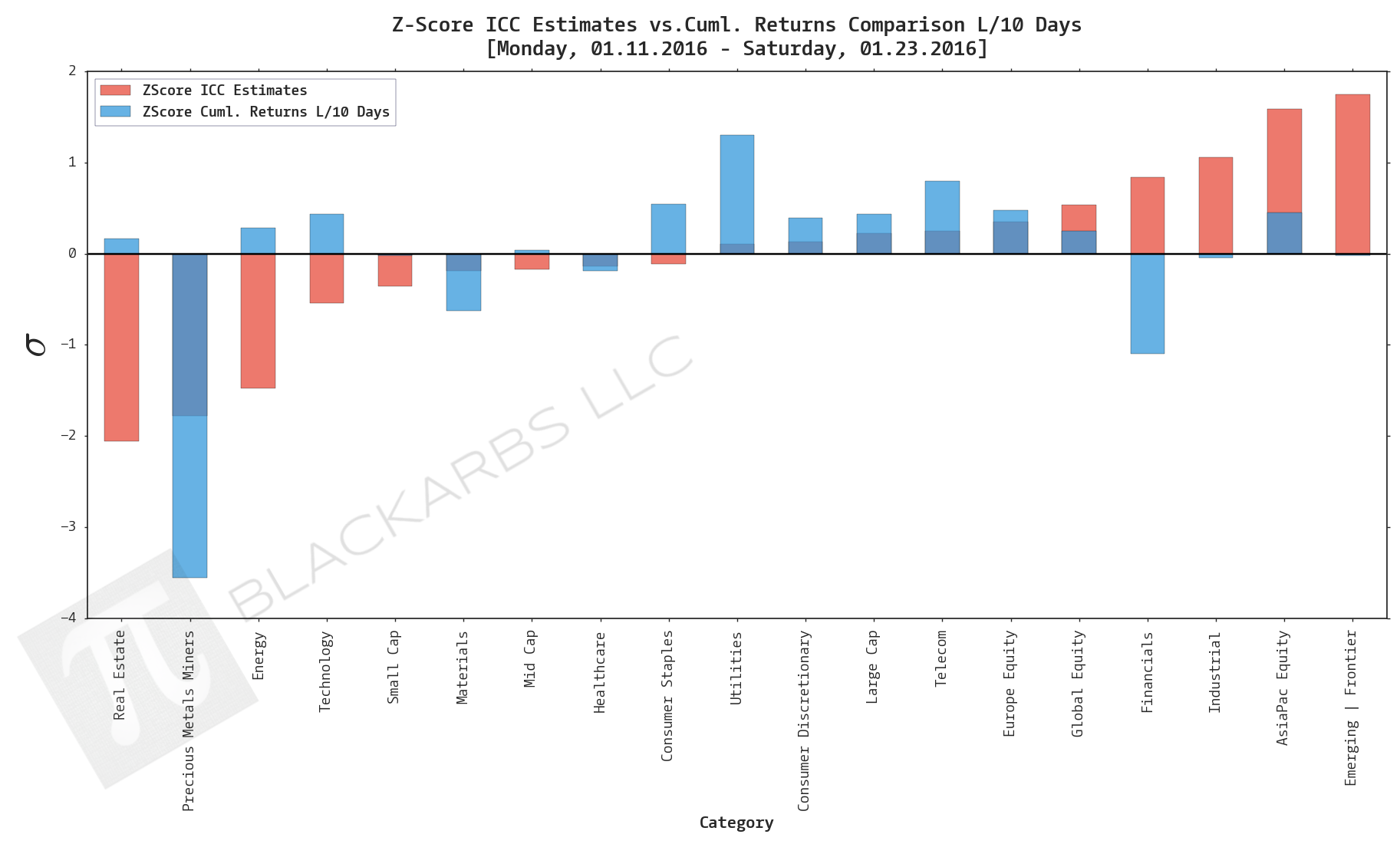

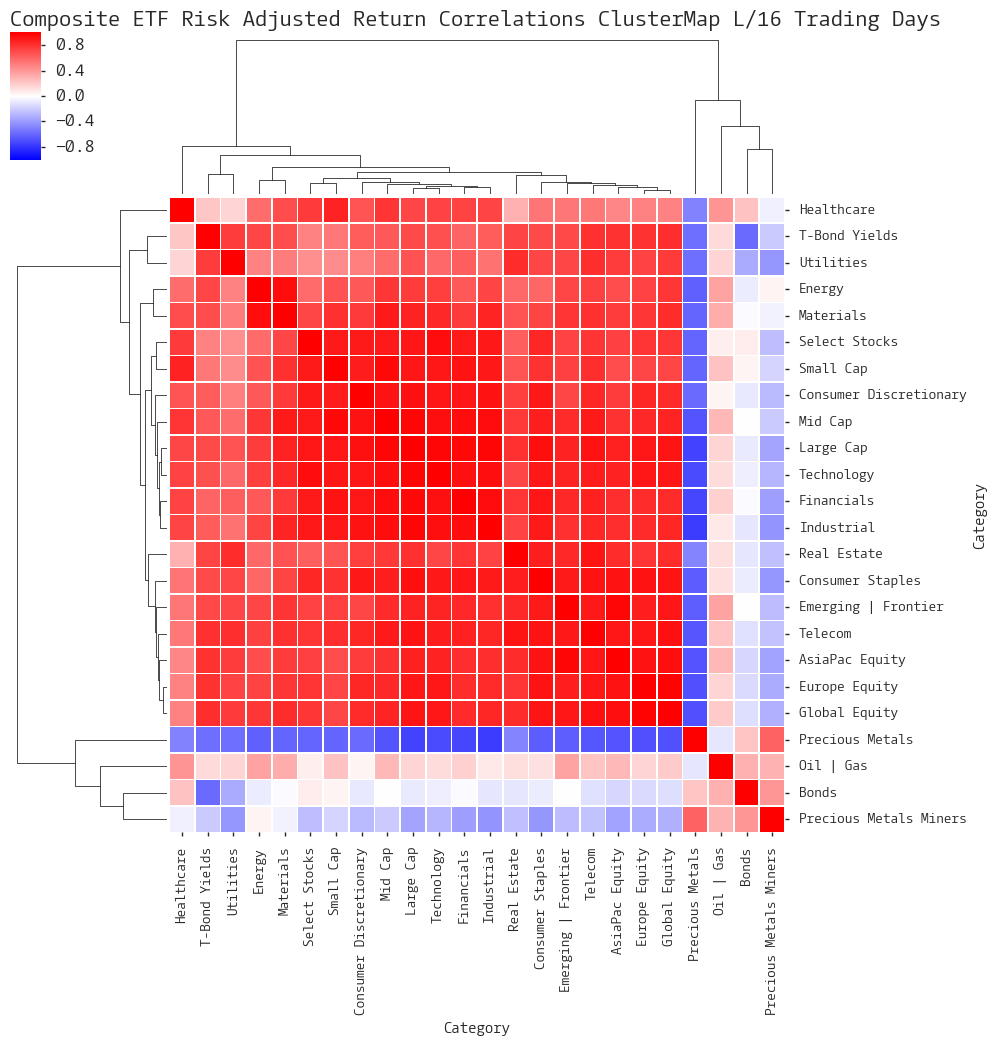

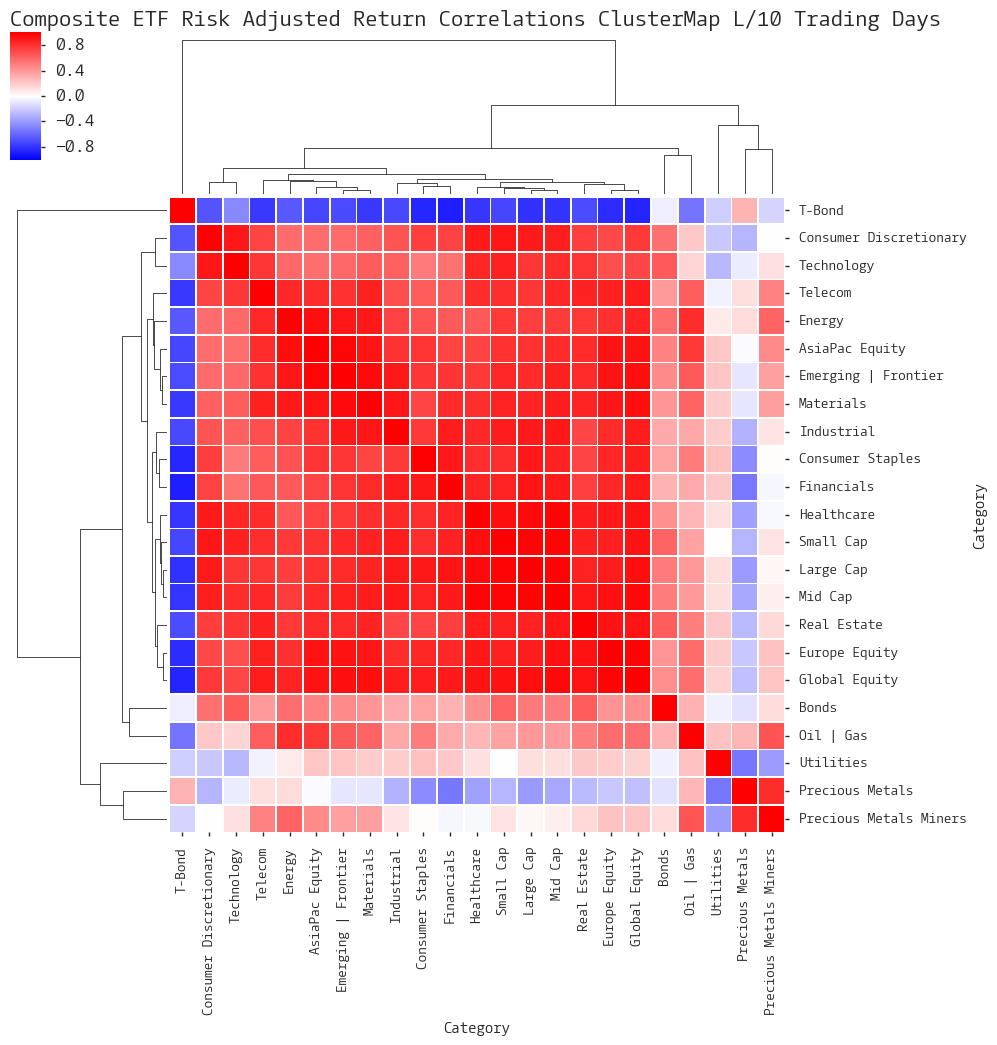

#block-yui_3_17_2_4_1455394346404_17847 .social-icons-style-border .sqs-svg-icon--wrapper { box-shadow: 0 0 0 2px inset; border: none; } FOR A DEEPER DIVE INTO ETF PERFORMANCE AND RELATIVE VALUE SUBSCRIBE TO THE ETF INTERNAL ANALYTICS PACKAGE HERE LAYOUT (Organized by Time Period): Composite ETF Cumulative Returns Momentum Bar plot Composite ETF Cumulative Returns Line plot Composite ETF Risk-Adjusted Returns Scatter plot (Std vs Mean) Composite ETF Risk-Adjusted Return Correlations

READ MORE →