PythonGlobal Markets

COMPOSITE MACRO ETF WEEKLY ANALYTICS (4/09/2016)

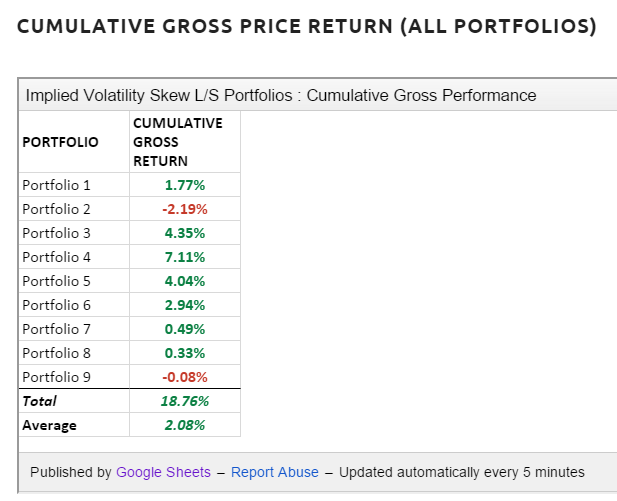

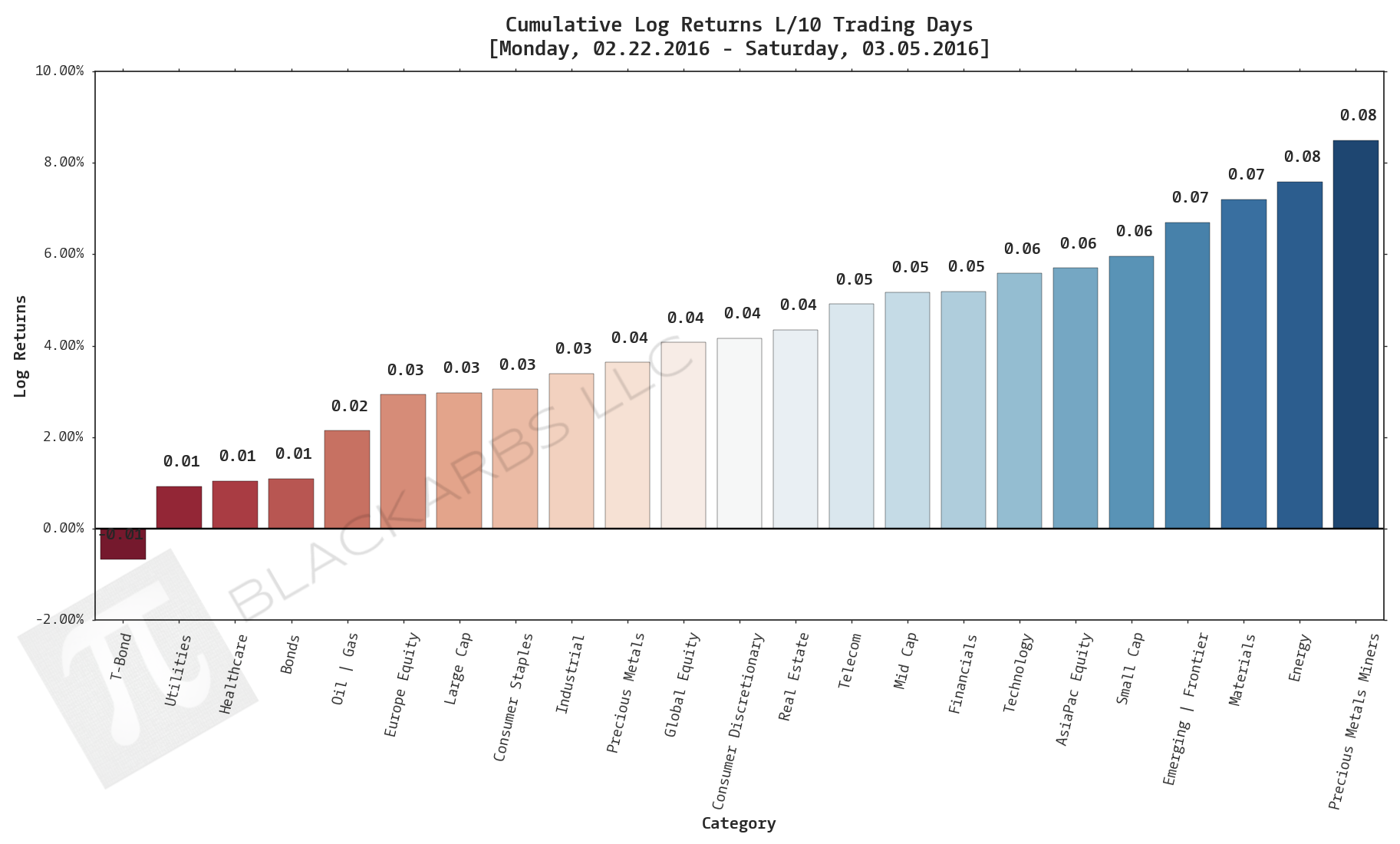

Blog RSS FOR A DEEPER DIVE INTO ETF PERFORMANCE AND RELATIVE VALUE SUBSCRIBE TO THE ETF INTERNAL ANALYTICS PACKAGE HERE LAYOUT (Organized by Time Period): Composite ETF Cumulative Returns Momentum Bar plot Composite ETF Cumulative Returns Line plot Composite ETF Risk-Adjusted Returns Scatter plot (Std vs Mean) Composite ETF Risk-Adjusted Return Correlations Heatmap (Clusterplot) Implied Cost of Capital Estimates Composite ETF Cumulative Return Tables Notable Trends and Observati

READ MORE →