PythonQuant

Institutional Level Long/Short Strategies in Quantopian (OCF/EV)

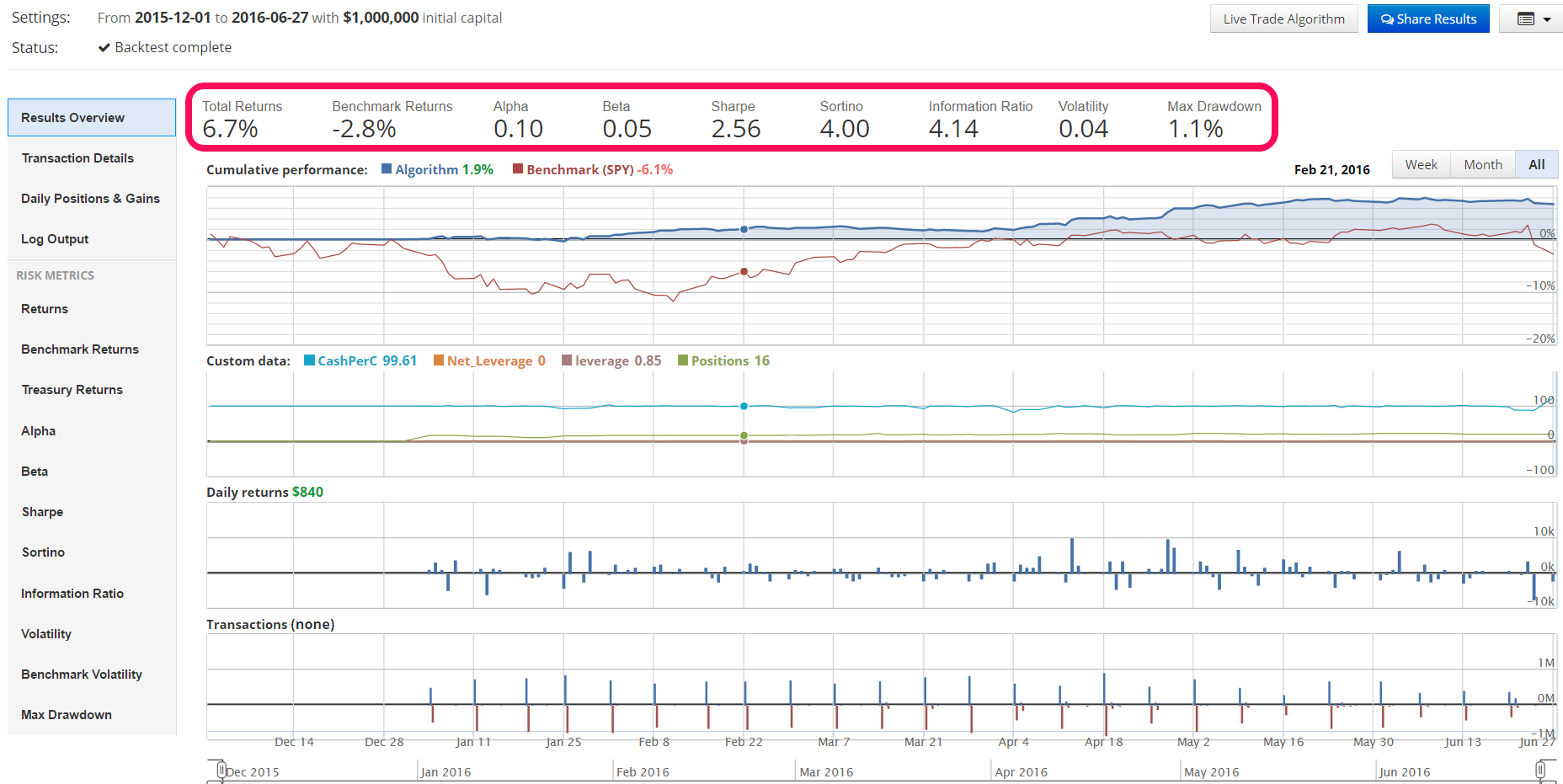

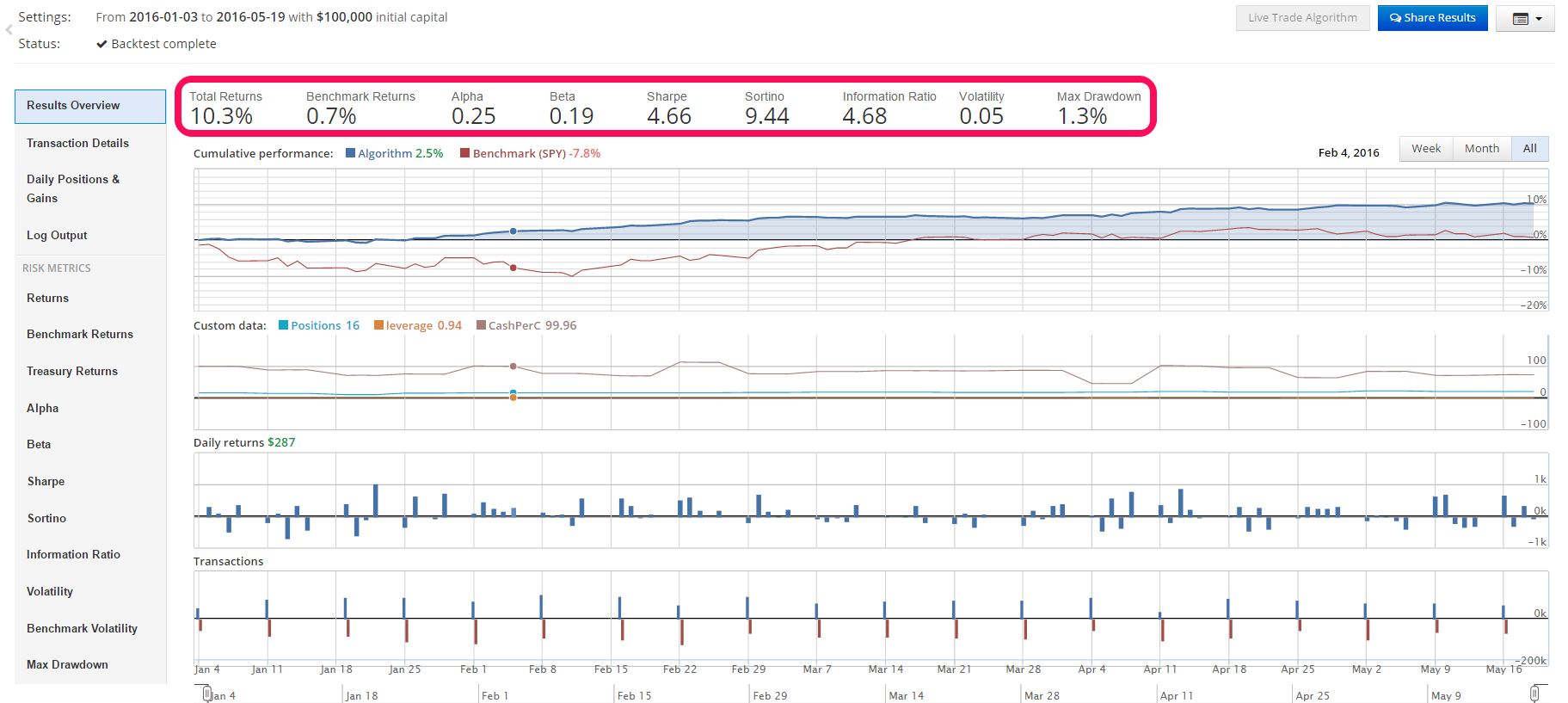

Post Outline * Background * Strategy Summary * Implementation Details * Strategy Results and Analysis * References (Notes) Background Recently I was blessed with an introduction to S&P Global-Market Intelligence's Director of Business Development, Matt Morrissy and gifted a trial membership to the S&P Capital IQ platform [1]. Specifically, I was given an opportunity to review and provide feedback for their "Alpha Factor Library." Their team, the Quantamental Group [2], has researched an

READ MORE →