PythonQuant

Backtesting the Implied Volatility Long/Short Strategy (10/18/16)

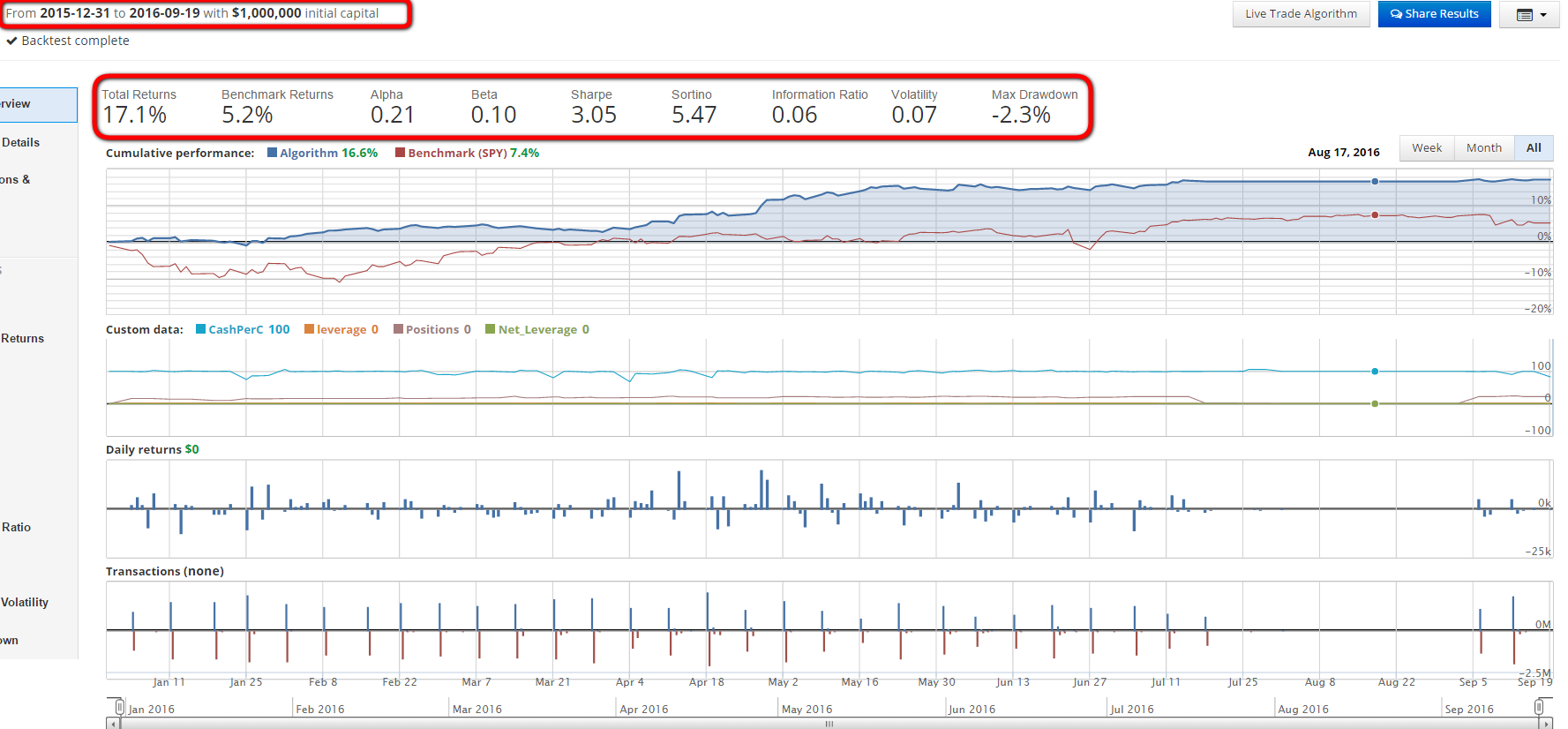

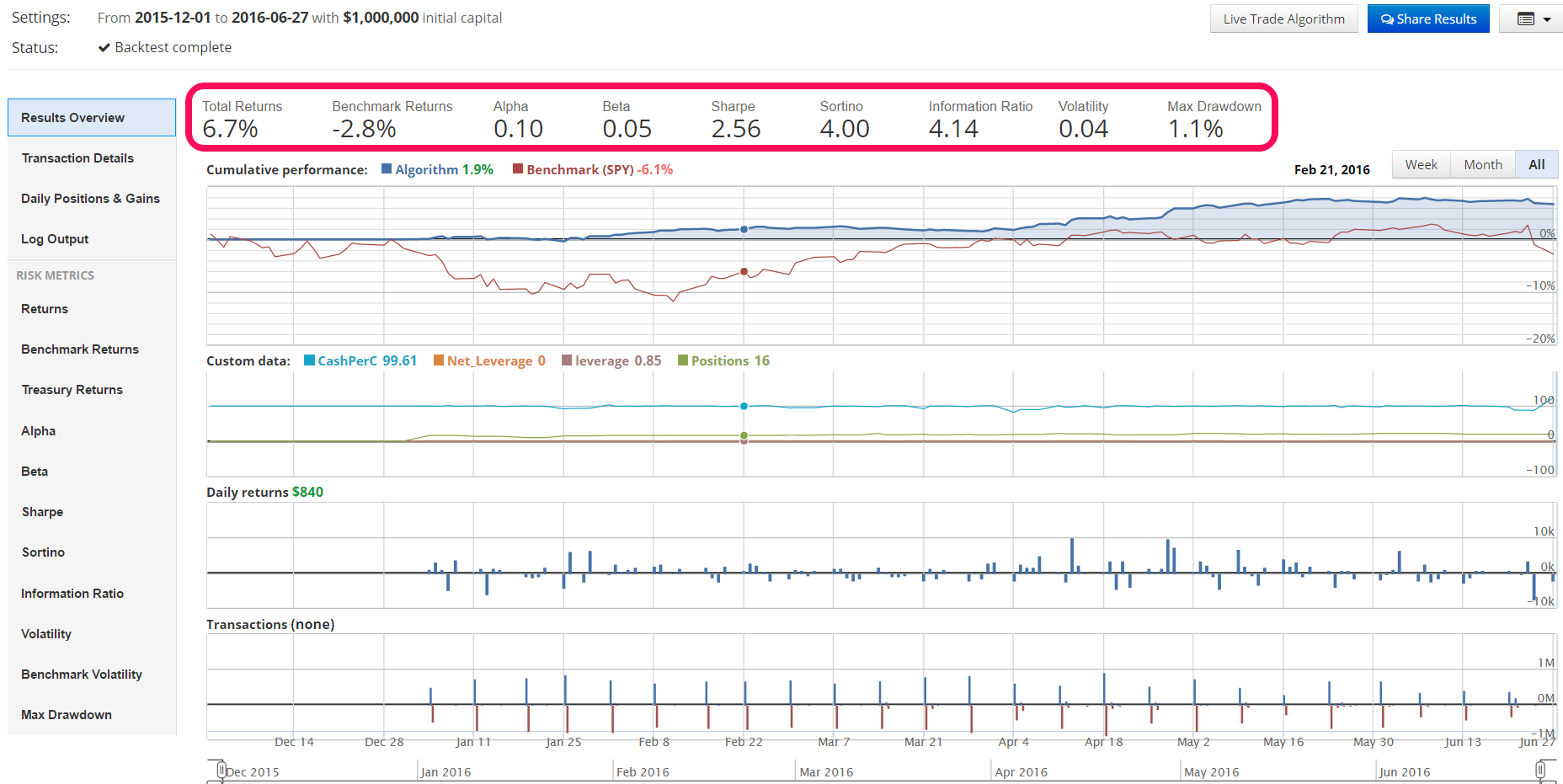

Post Outline * Strategy Summary * References * 4-Week Holding Period Strategy Update * 1-Week Holding Period Strategy Updated (Target Leverage=2) Strategy Summary This is a stylized implementation of the strategy described in the research paper titled "What Does Individual Option Volatility Smirk Tell Us About Future Equity Returns" by Yuhang Xing, Xiaoyan Zhang and Rui Zhao. The authors show that their SKEW factor predicts individual equity returns up to 6 months! ABSTRACT Stocks exhi

READ MORE →