Equity AnalysisPython

Could SPY ETF Component Participation Have Alerted Us to Sell (Hedge) Prior to the Recent Market Downturn?

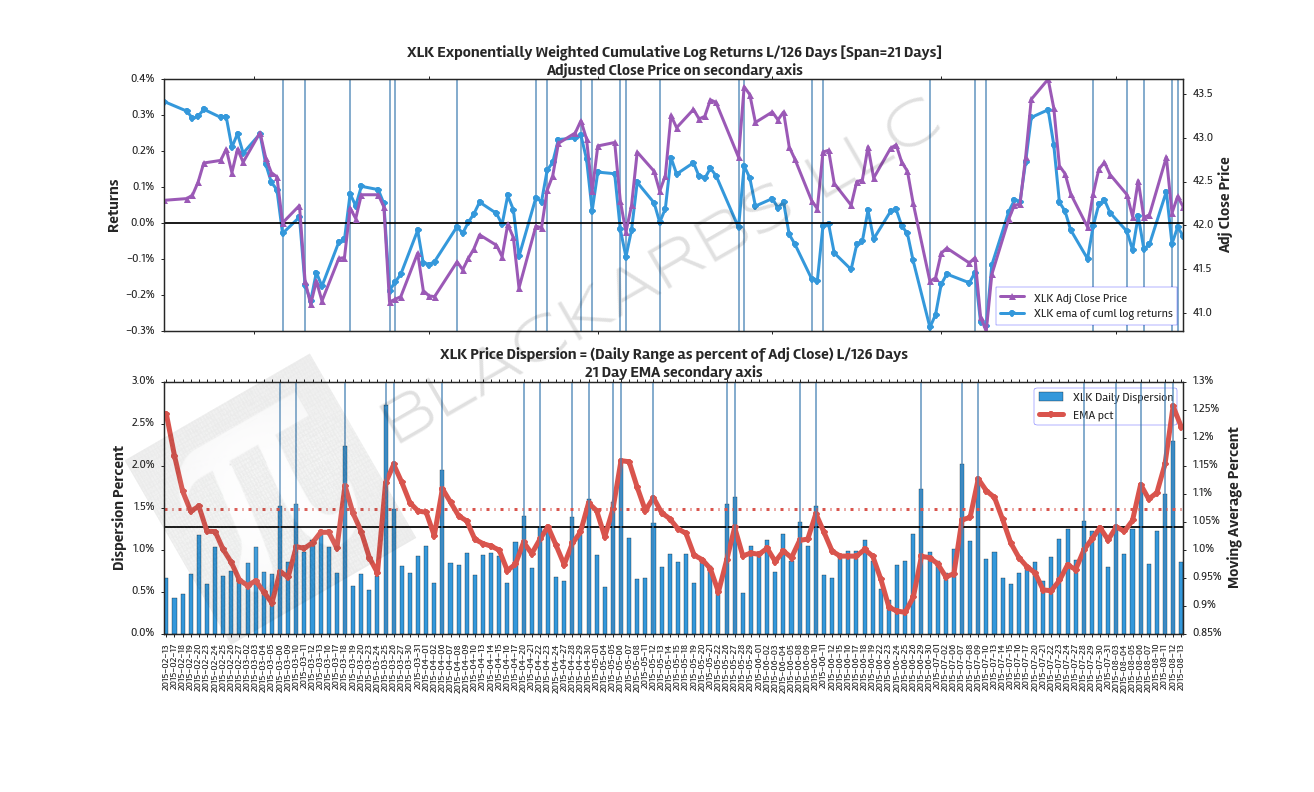

This is the Python Code version of a guest post presented here on RectitudeMarket.com. If you would like to read the analysis without the Python code please click the link above. To market pundits and casual observers the recent correction in equity markets appeared as a surprise. Overall headline economic data was positive at best and mixed at worst. Domestically, capital markets had been looking ‘ok’ while most of the major volatility was taking place abroad in emerging markets, and commodity

READ MORE →