Global MarketsPython

COMPOSITE MACRO ETF WEEKLY ANALYTICS (10/31/2015)

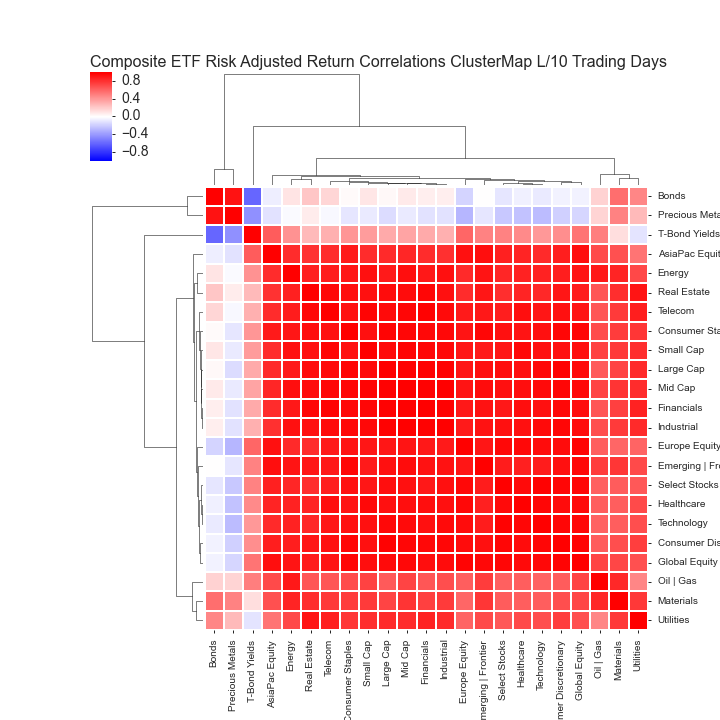

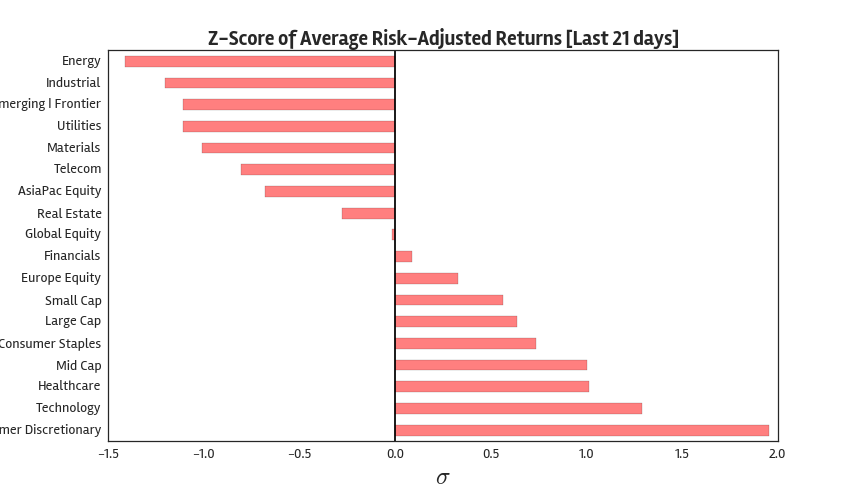

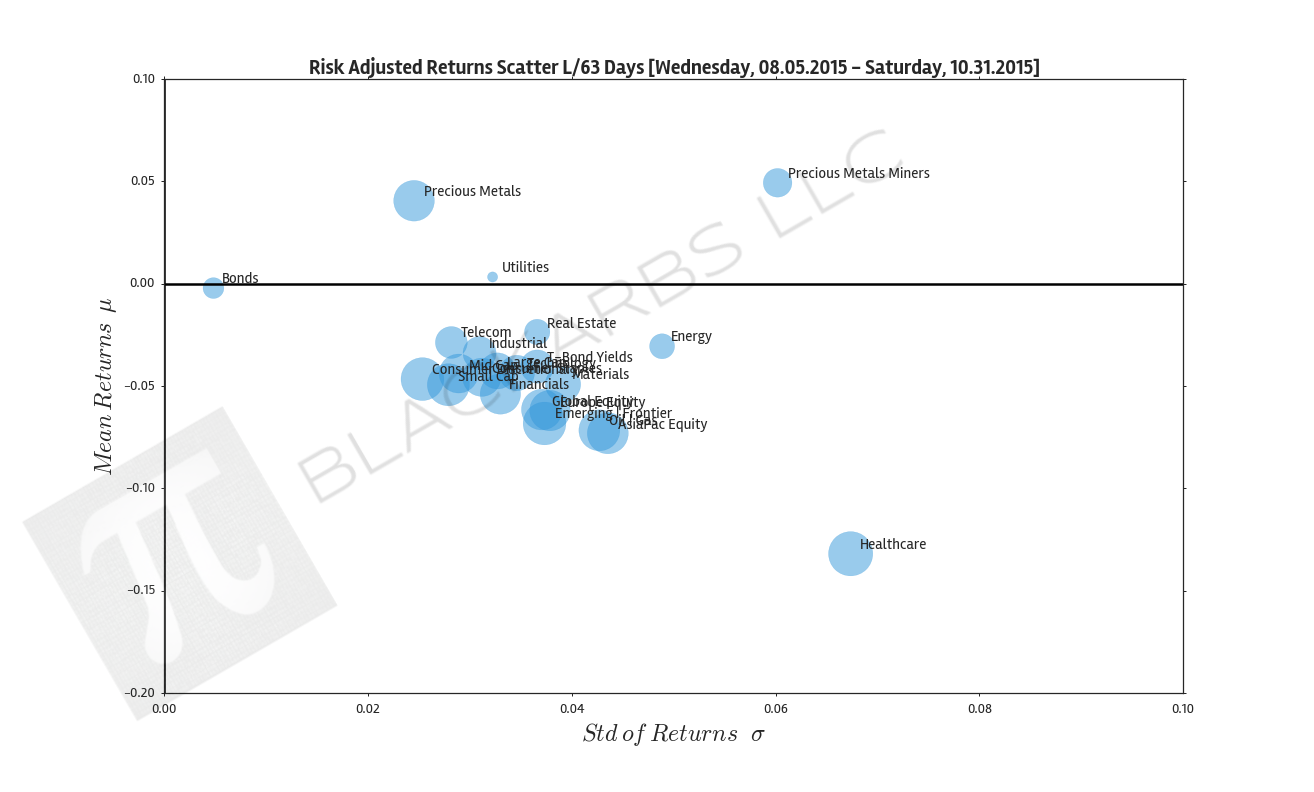

NEW LAYOUT: Going forward I will be testing a new organizational format for the charts. I have created a chart description page which details how each plot type is commonly interpreted (used). I will provide a link to the chart description page in the caption of each chart. The primary change is all the chart types will be grouped by the referenced time period. It is my hope that grouping the data this way will allow for easier analysis. Each time period grouping will display the charts in the

READ MORE →