AWSCloud

AWS Trading Part 2 - The Strategy

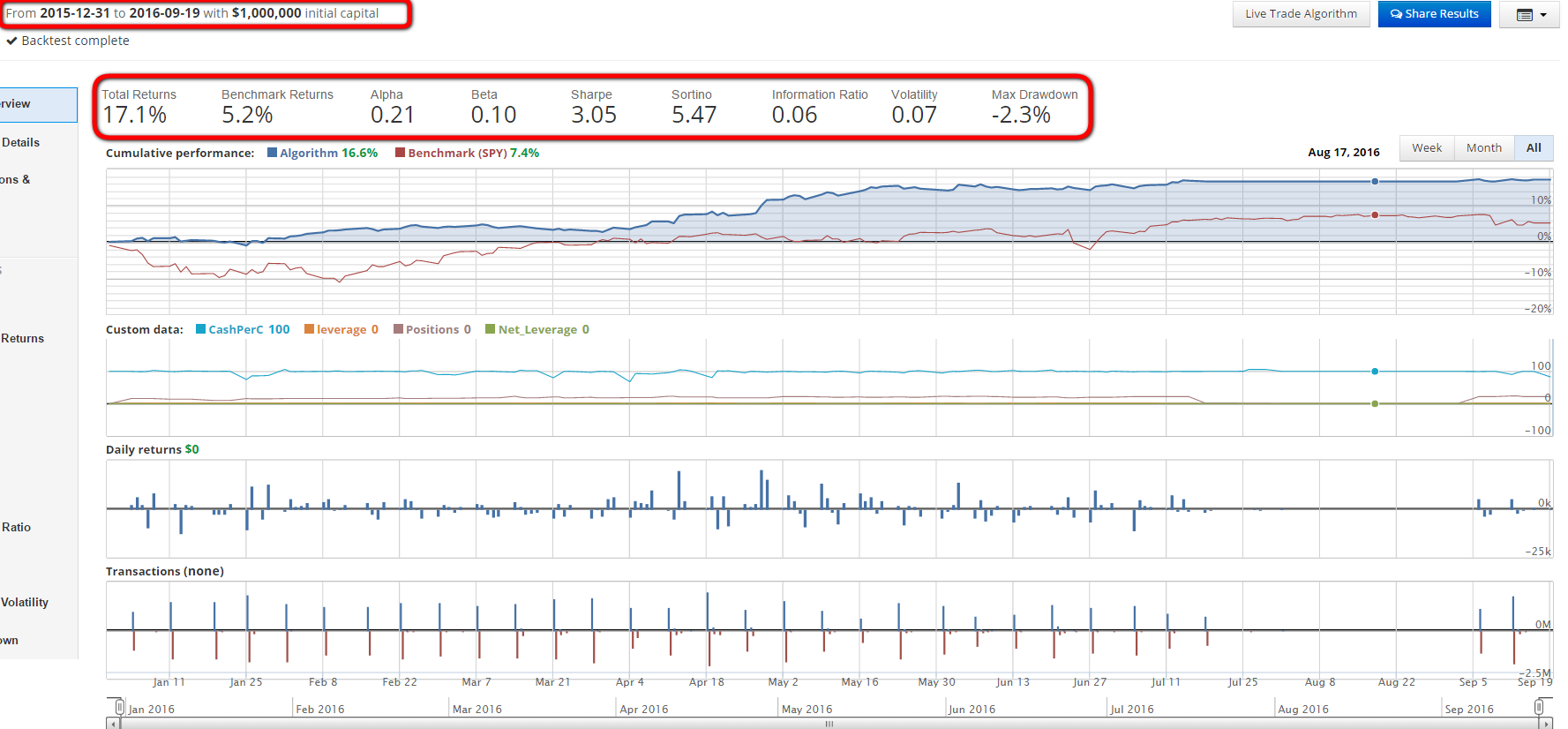

The code and diagrams for the strategy can be found on github. AWS Trading Part 2 Youtube video is here. Introduction In part 1 youtube video link we covered the data pipeline portion of the AWS trading bot architecture. I demonstrated how to set up your AWS environment, including creating a simple dynamoDB database to hold our price and strategy data. Then we walked through the data pipeline code in detail including how to grab the data and populate our db with it. In this post we’ll cover t

READ MORE →