Deconstructing a Failed Strategy: Was Anything Worth Saving?

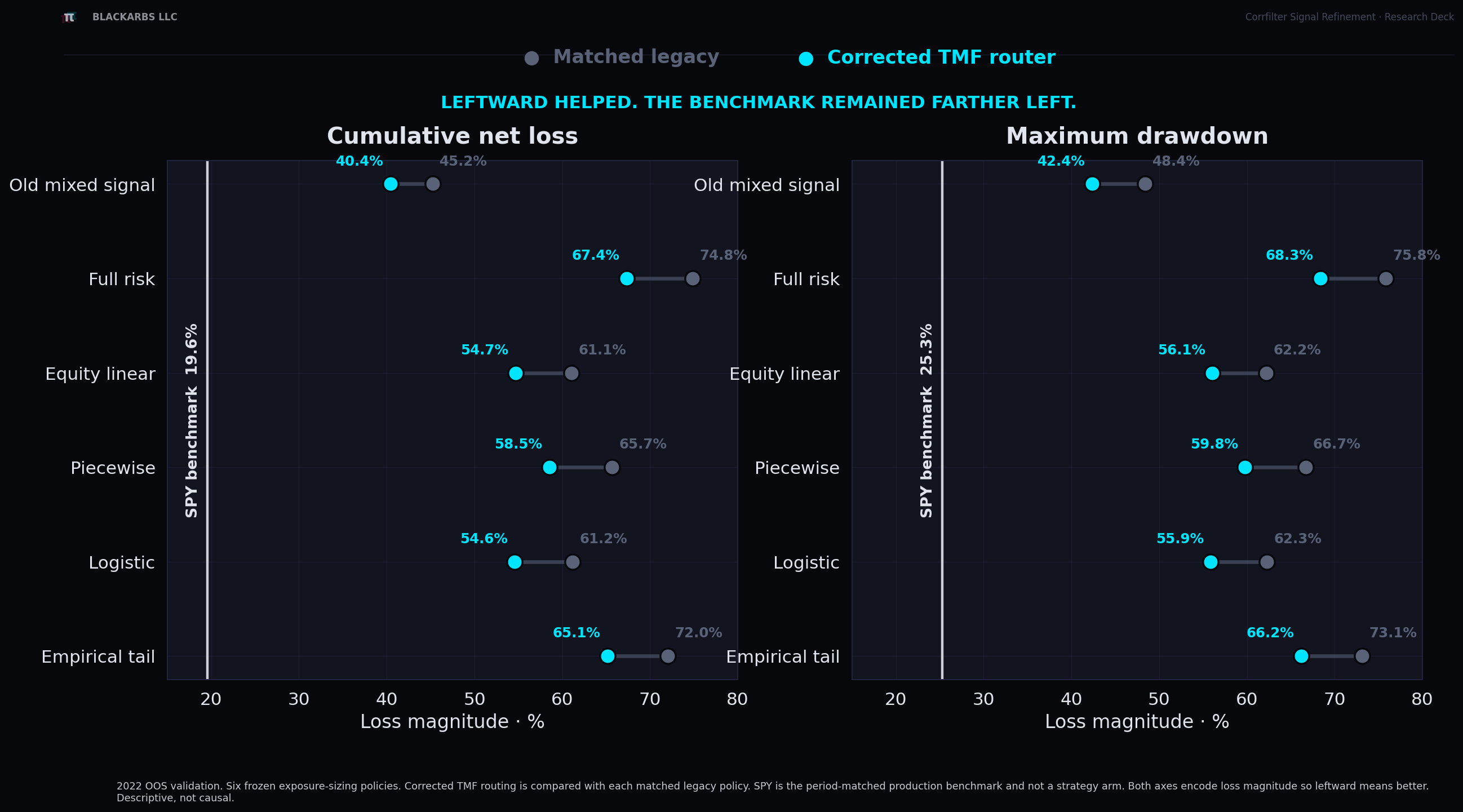

A strategy redesign looked dramatically better in sample. A 2022 out-of-sample test exposed the hidden leverage, and the strategy was rejected before the final holdout.

READ MORE → A strategy redesign looked dramatically better in sample. A 2022 out-of-sample test exposed the hidden leverage, and the strategy was rejected before the final holdout.

READ MORE →

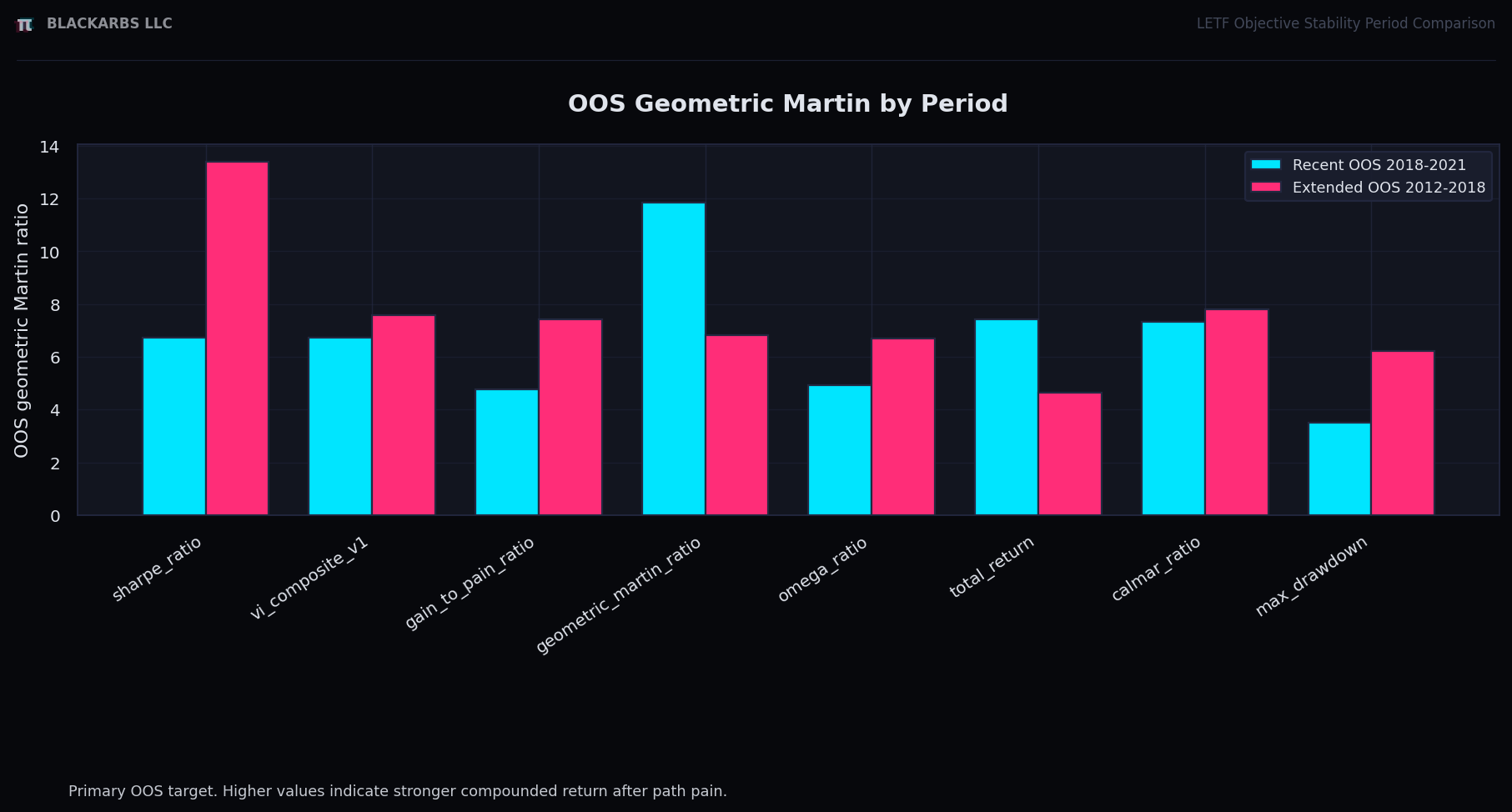

A walkforward optimizer objective test using geometric Martin as the out-of-sample path-quality judge.

READ MORE →

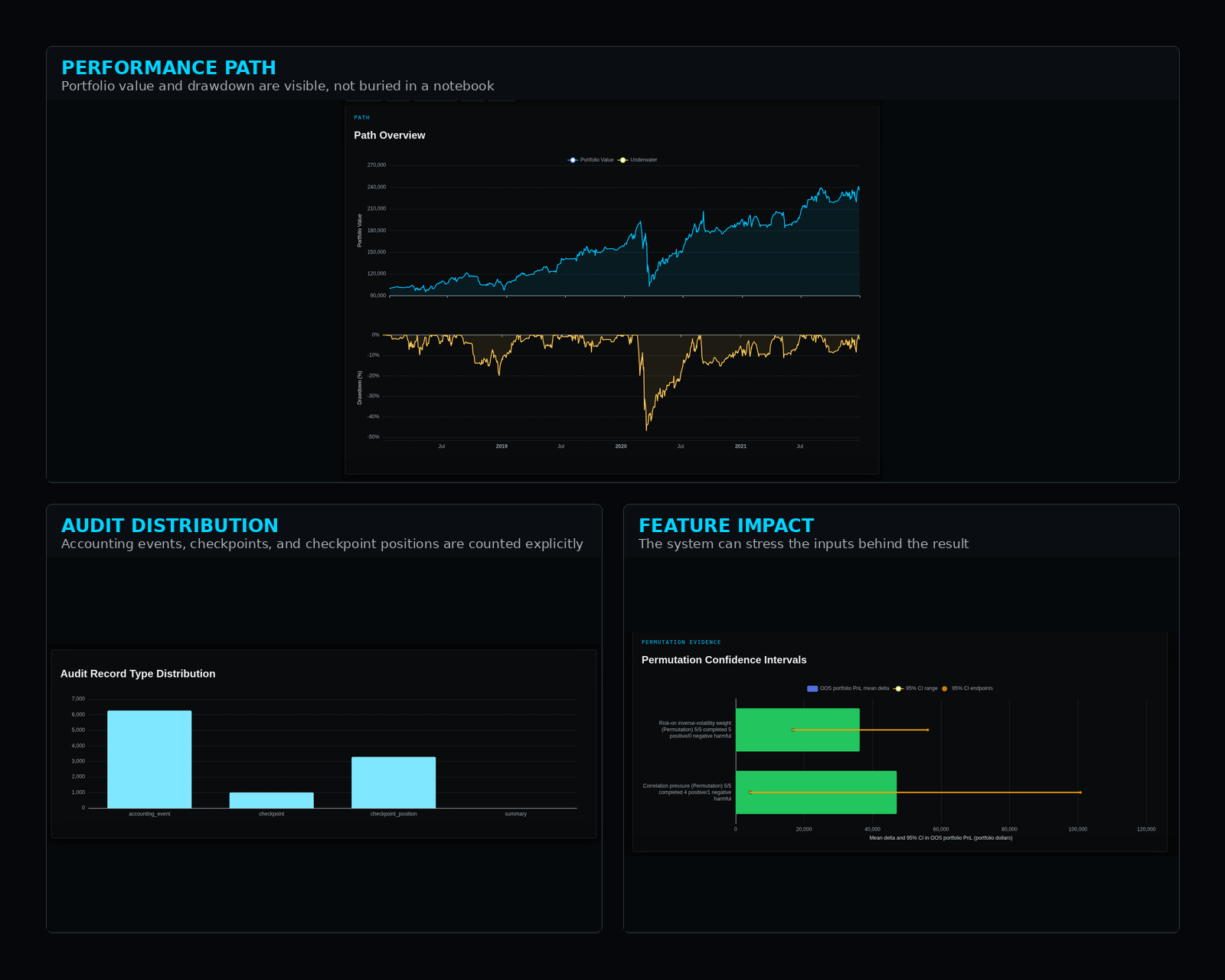

The first job of a serious research system is not to find alpha. It is to create the infrastructure where alpha can be trusted.

READ MORE →Three systems, one thesis: reliable judgment requires infrastructure.

READ MORE →The notebook taught you theory, but not how to deploy.

READ MORE →

The code and diagrams for the strategy can be found on github. AWS Trading Part 2 Youtube video is here. Introduction In part 1 youtube video link we covered the data pipeline portion of the AWS trading bot architecture. I demonstrated how to set up your AWS environment, including creating a simple dynamoDB database to hold our price and strategy data. Then we walked through the data pipeline code in detail including how to grab the data and populate our db with it. In this post we’ll cover t

READ MORE →

I just published Part 1 of my new YouTube series, and I'm excited to share it with you all! After my recent post about automating trading strategies with AWS Cloud, many of you asked for a deeper dive into the technical implementation. Well, here it is! What's in Part 1? In this first video, we're tackling the foundation: configuring your AWS data pipeline and writing the Python code to make it all work. I walk through the exact steps I use in my own automated trading system, showing you how

READ MORE →

This year I launched a strategy subscription service for a long-only ETF strategy developed in house. I learned a lot through this process but I made several mistakes that pushed me to learn new skills and improve the product offering. In this series I will discuss my initial mistakes, and how correcting them led me to automate the system using AWS cloud and how you can too. Mistake #1 First mistake was not considering automation in the beginning. I had the script, I ran it daily, used the s

READ MORE →

Join the growing Blackarbs Research Group Discord community here Get access to the strategy that has returned 48% live trading since November 2023 here (Updated: 2024-Mar-02) Recap In part 1 of the series, I introduced the blackarbs retirement algorithm, a long only leveraged ETF strategy meant to perform at or better than SPY (the market benchmark) with less volatility. I discussed the goals I set for the algo and how thus far in simulated backtests and live trading it has met those goals.

READ MORE →

Join the growing Blackarbs Research Group Discord community here Get access to the strategy that has returned 48% in live trading since this article was written here (Updated: 2024-Mar-02) Mission Recap Blackarbs current mission is to create automated strategies with the goal of beating the market with superior risk adjusted returns. Originally, I wanted to illuminate some of the more hidden aspects of markets and investing that I found interesting and of value. Over time, that goal crystall

READ MORE →

Introduction This is an old concept concerning the opening range. The idea is that the opening range often sets the day’s high or low within the first hour of cash equities trading (9:30 am - 10:30 am EST). Recently a trader on Youtube made the claim that you can know with 88% probability the high or low of the day after the first hour of trading. He managed to successfully repopularize the idea of using the opening range in a a more specific way than other methods. In this article I set out t

READ MORE →