ResearchQuant

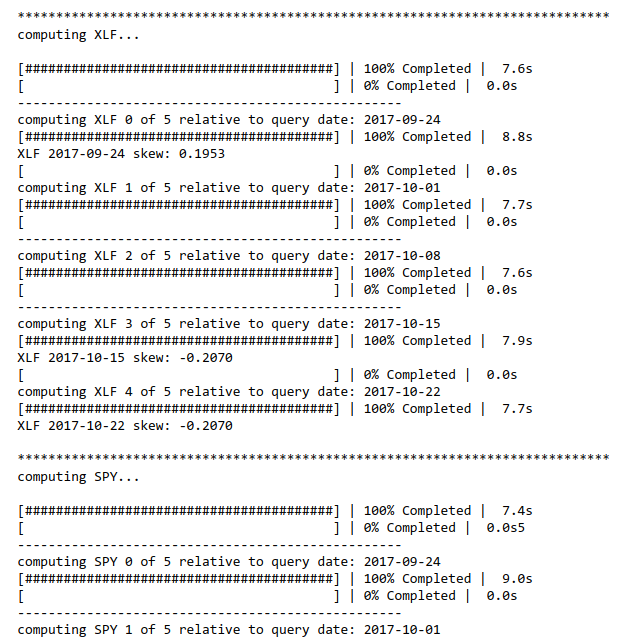

Computing Option Skews with Dask

Post Outline * Introduction * Links + Datasets * Notebook * Next Steps Introduction This article series provides an opportunity to move towards more interactive analysis. My plan is to integrate more Jupyter notebooks and Github repos into my research/publishing workflow. For datasets that are too big to share through github I will provide a download link both here and in the github readme. I will be posting the notebooks into this blog using iframes. If you experience any issues with f

READ MORE →