PythonQuant

A Dead Simple 2-Asset Portfolio that Crushes the S&P500 (Part 2)

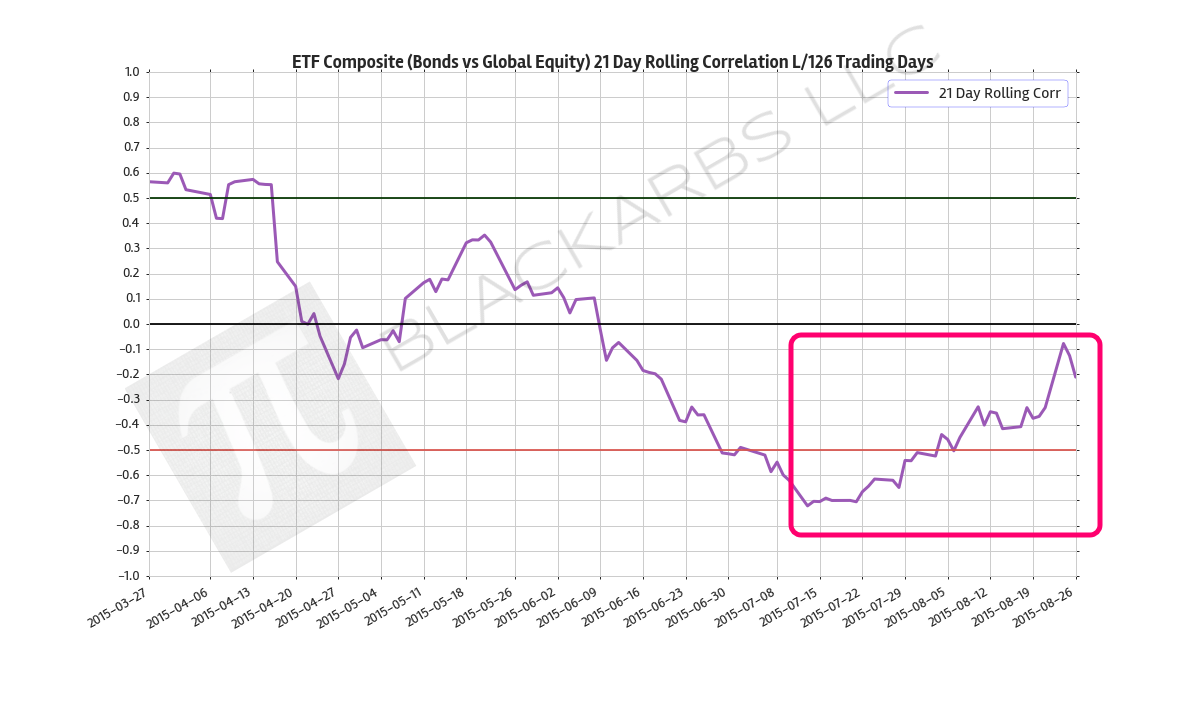

In Part 1, and Part 1.5 I introduced a simple 2-asset portfolio that substantially outperformed the SPY ETF since 2009. In Part 1 I examined the performance of an "inverse risk-parity" approach where the ETF with the largest volatility contribution to the portfolio was weighted more heavily. In Part 1.5 I examined the performance of the actual "risk-parity" approach, where the ETF with the smallest volatility contribution is weighted more heavily. In this post I will examine some of the conceptu

READ MORE →