PythonQuant

Synthetic ETF Data Generation (Part-2) - Gaussian Mixture Models

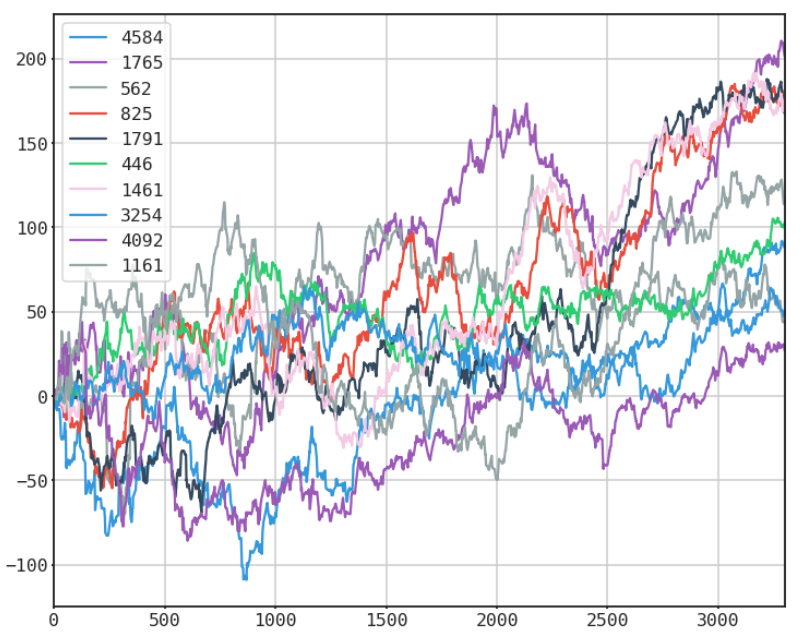

This post is a summary of a more detailed Jupyter (IPython) notebook where I demonstrate a method of using Python, Scikit-Learn and Gaussian Mixture Models to generate realistic looking return series. In this post we will compare real ETF returns versus synthetic realizations. To evaluate the similarity of the real and synthetic returns we will compare the following: * visual inspection * histogram comparisons * descriptive statistics * correlations * autocorrelations The data set we will

READ MORE →