PythonQuant

Asset Pricing using Extreme Liquidity Risk with Python (Part-1)

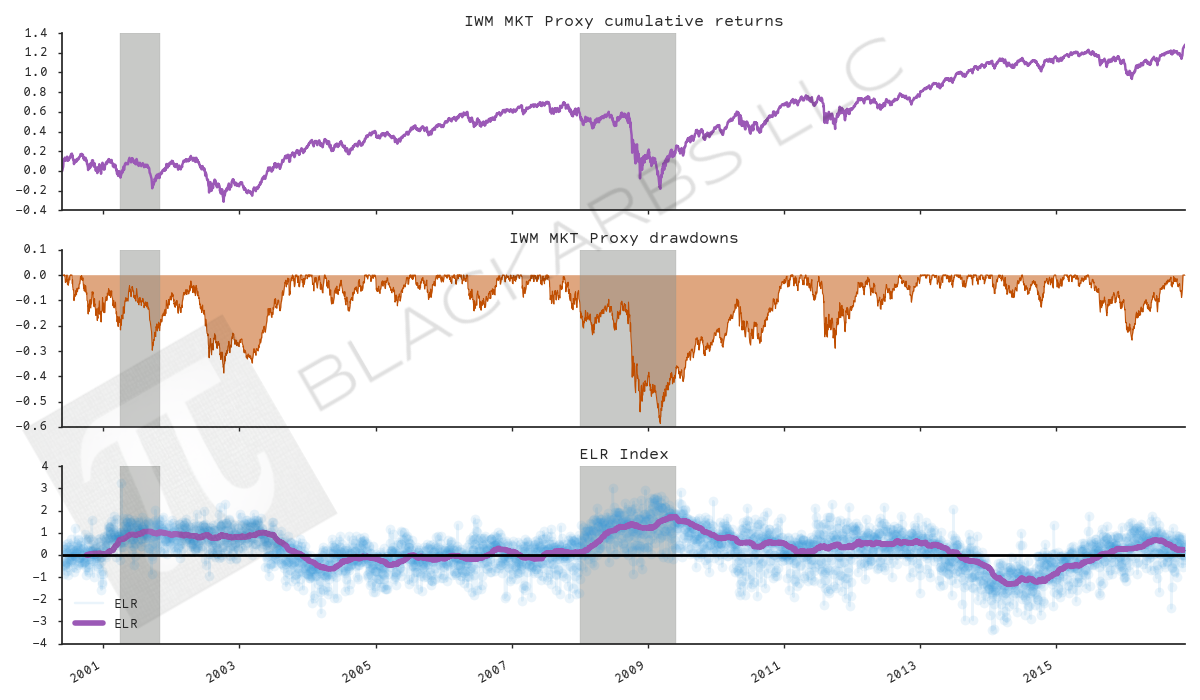

Post Outline * Introduction * Get Data * Calculate Cross-Sectional Extreme Liquidity Risk * Quick and Dirty Observations * Next Steps * References iNTRODUCTION One of the primary goals of quantitative investing is effectively managing tail risk. Failure to do so can result in crushing drawdowns or a total blowup of your fund/portfolio. Commonly known tools for estimating tail risk, e.g. Value-at-Risk, often underestimate the likelihood and magnitude of risk-off events. Furthermore, tai

READ MORE →