COMPOSITE MACRO ETF WEEKLY ANALYTICS (2/06/2016)

/FOR A DEEPER DIVE INTO ETF PERFORMANCE AND RELATIVE VALUE SUBSCRIBE TO THE ETF INTERNAL ANALYTICS PACKAGE HERE

LAYOUT (Organized by Time Period):

Composite ETF Cumulative Returns Momentum Bar plot

Composite ETF Cumulative Returns Line plot

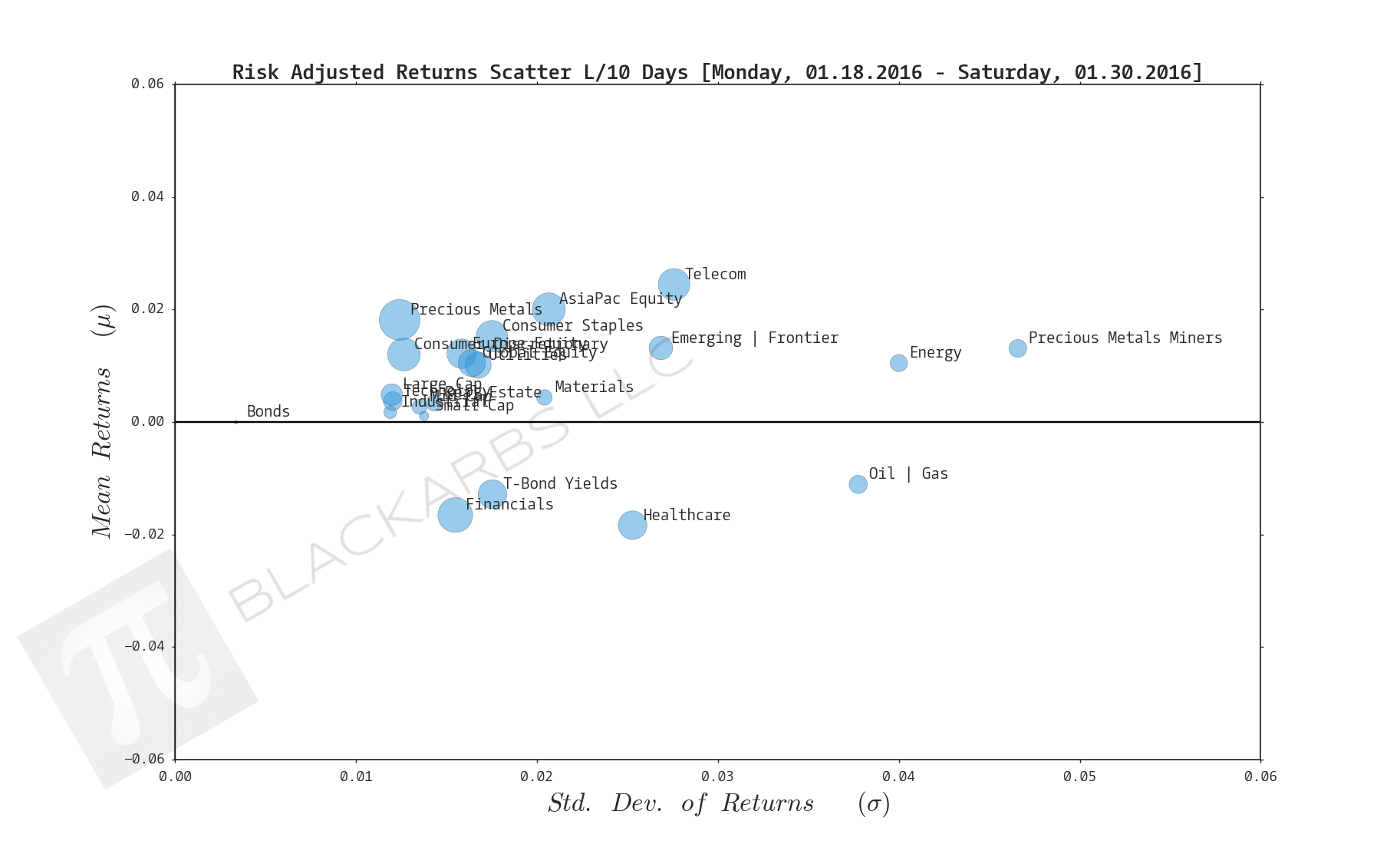

Composite ETF Risk-Adjusted Returns Scatter plot (Std vs Mean)

Composite ETF Risk-Adjusted Return Correlations Heatmap (Clusterplot)

Implied Cost of Capital Estimates

Composite ETF Cumulative Return Tables

Notable Trends and Observations

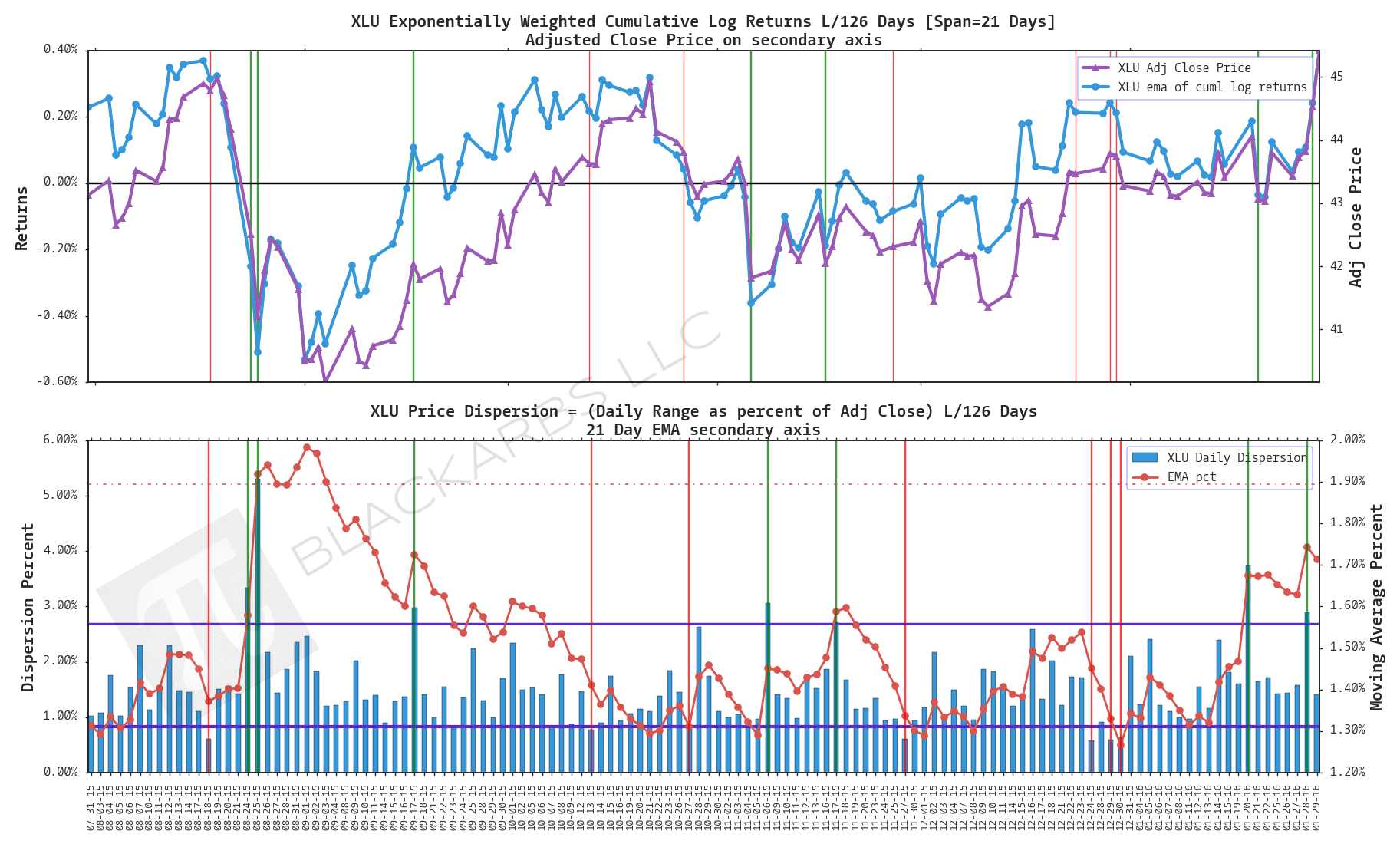

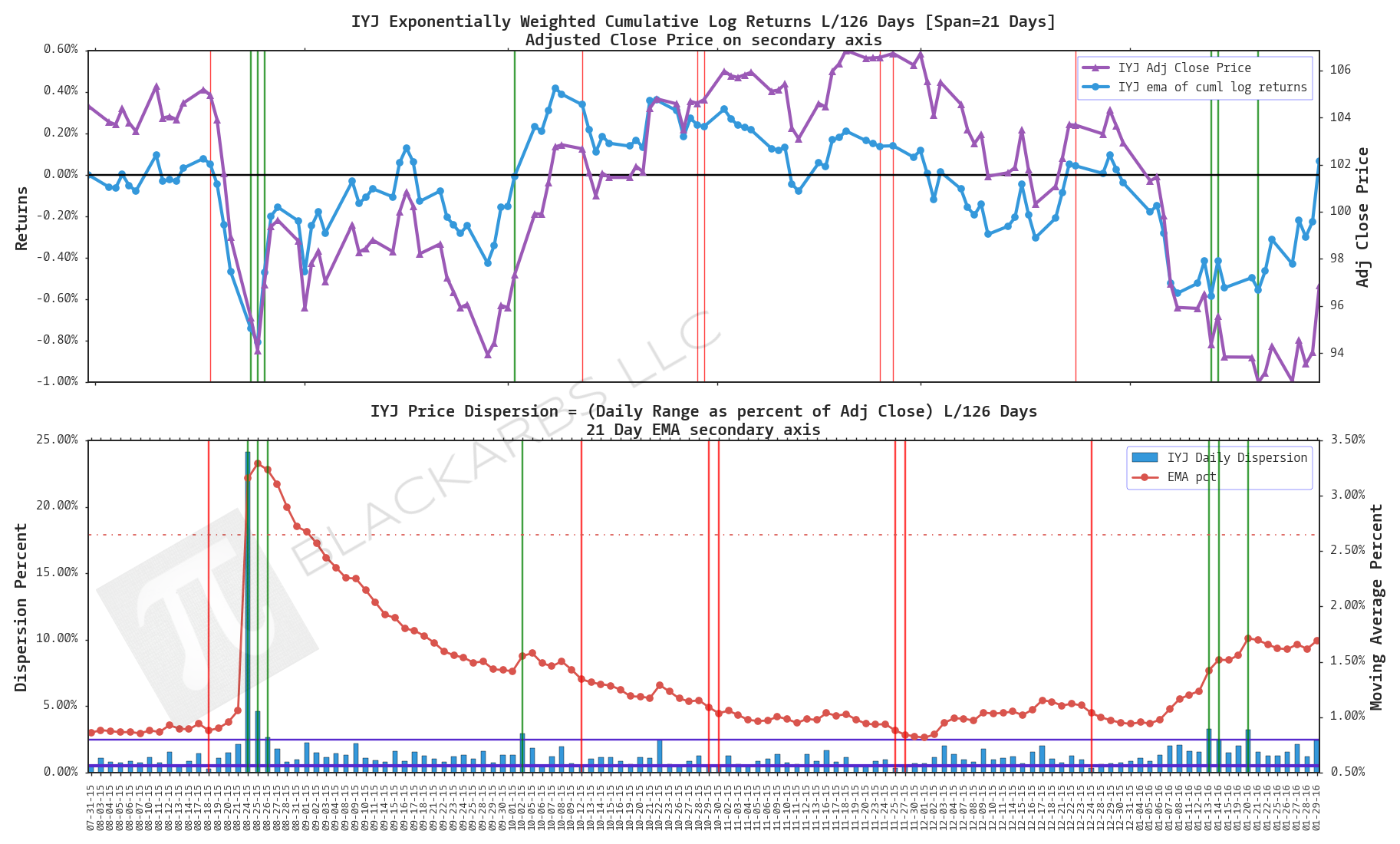

COMPOSITE ETF COMPONENTS:

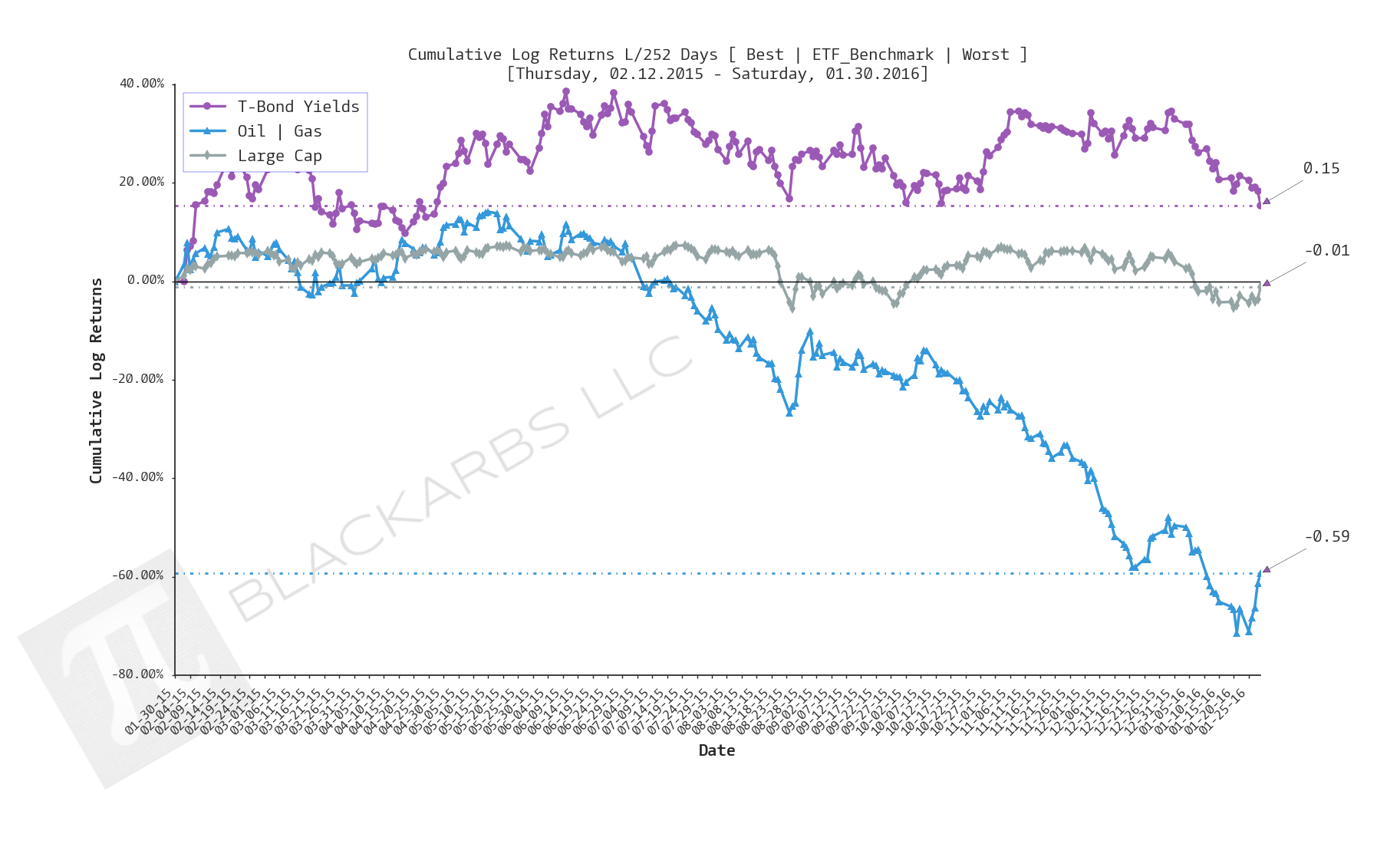

LAST 252 TRADING DAYS

LAST 126 TRADING DAYS

LAST 63 TRADING DAYS

LAST 21 TRADING DAYS

LAST 10 TRADING DAYS

Implied Cost of Capital Estimates:

To learn more about the Implied Cost of Capital see here.

CATEGORY AVERAGE ICC ESTIMATES

ALL ETF ICC ESTIMATES BY CATEGORY

Cumulative Return Tables:

Notable Observations and Trends:

- Market crash risk is rising. What is currently a correction is showing the potential to become much worse.

- T-Bond Yields are the worst performers over the last 21 and 10 day periods. Recall that Bond yields and prices have an inverse relationship, meaning that Treasury Bonds are seeing a strong bid from the market.

- Precious Metal Miners and Precious Metals have been among the top 3 performers for 3 out of 5 time periods starting over the last 126 days. These composites are usually bid up as a form of crash protection when investors fear 1) systematic devaluation of the USD and other major currencies 2) global market crash.

- Utilities being among the top 3 performers across all time periods also support the rising crash risk that markets appear to be pricing in.