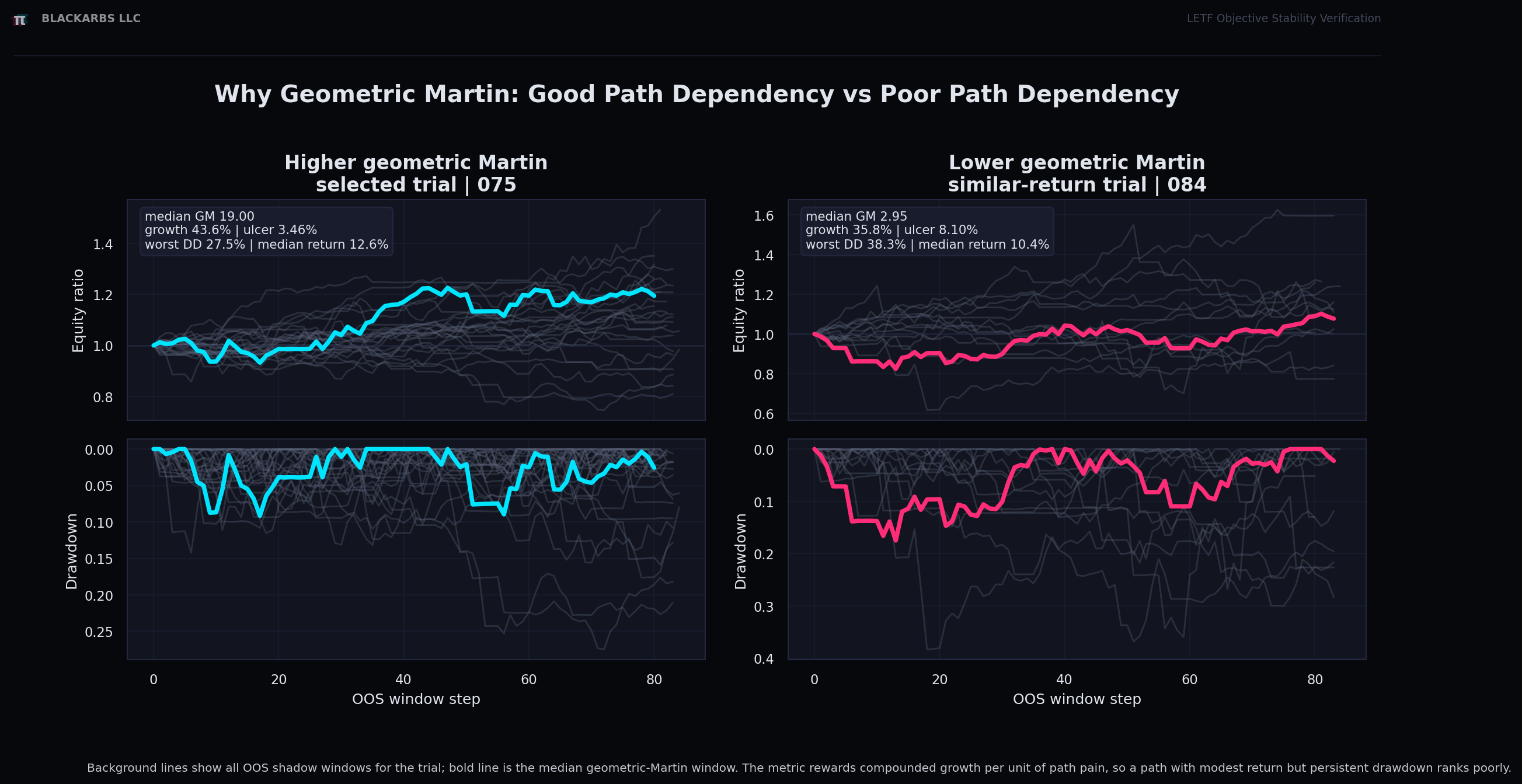

A good final return can hide a bad ride.

The highlighted windows finish with similar median returns, but very different path pain.

Which targets produced the best future paths?

This now includes geometric Martin as an optimizer target, not just as the OOS scoring rule.

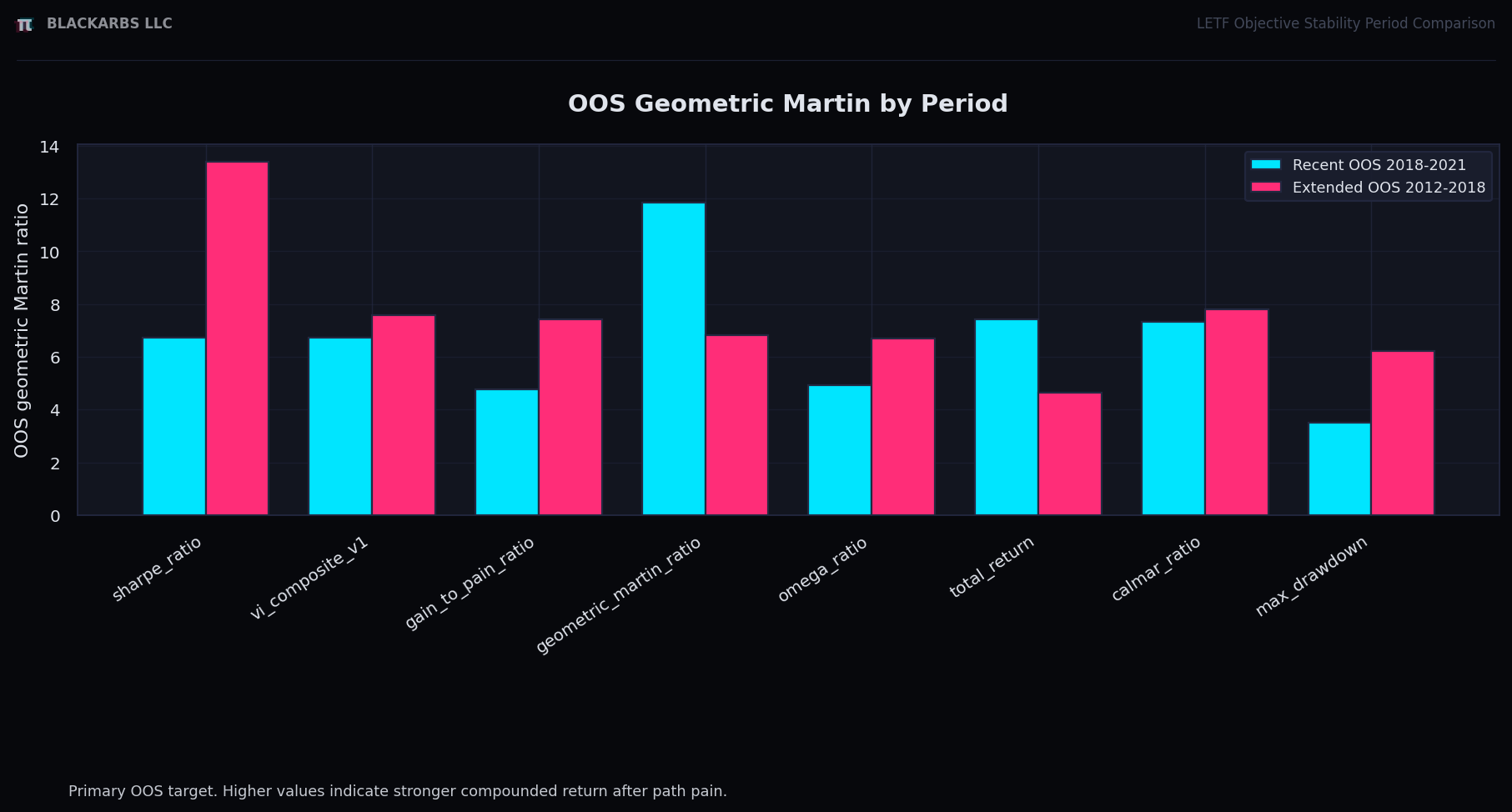

Did the ranking hold up when the future test got longer?

Top is best. The direct geometric-Martin objective did not stay ahead once the test period got longer.

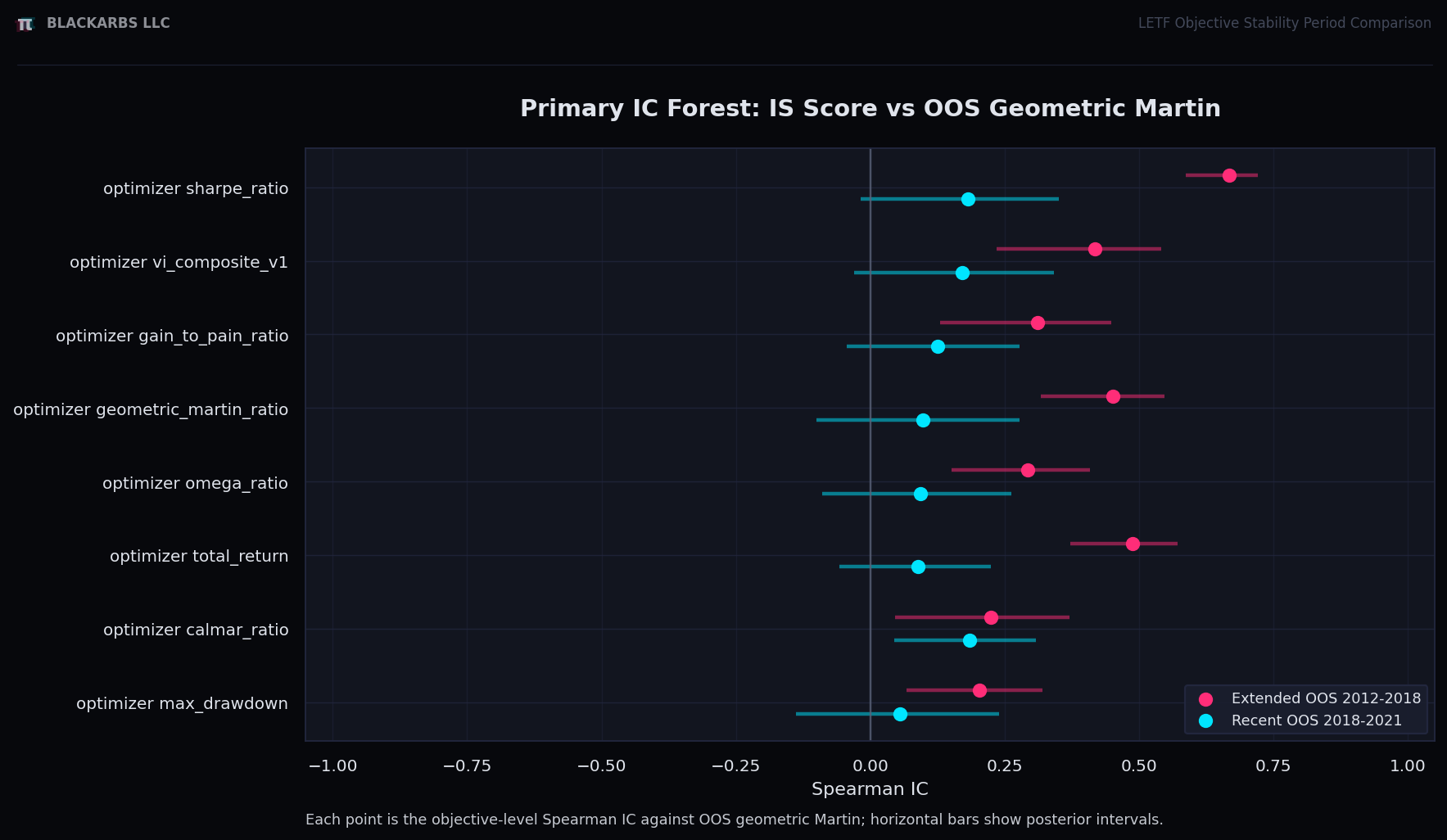

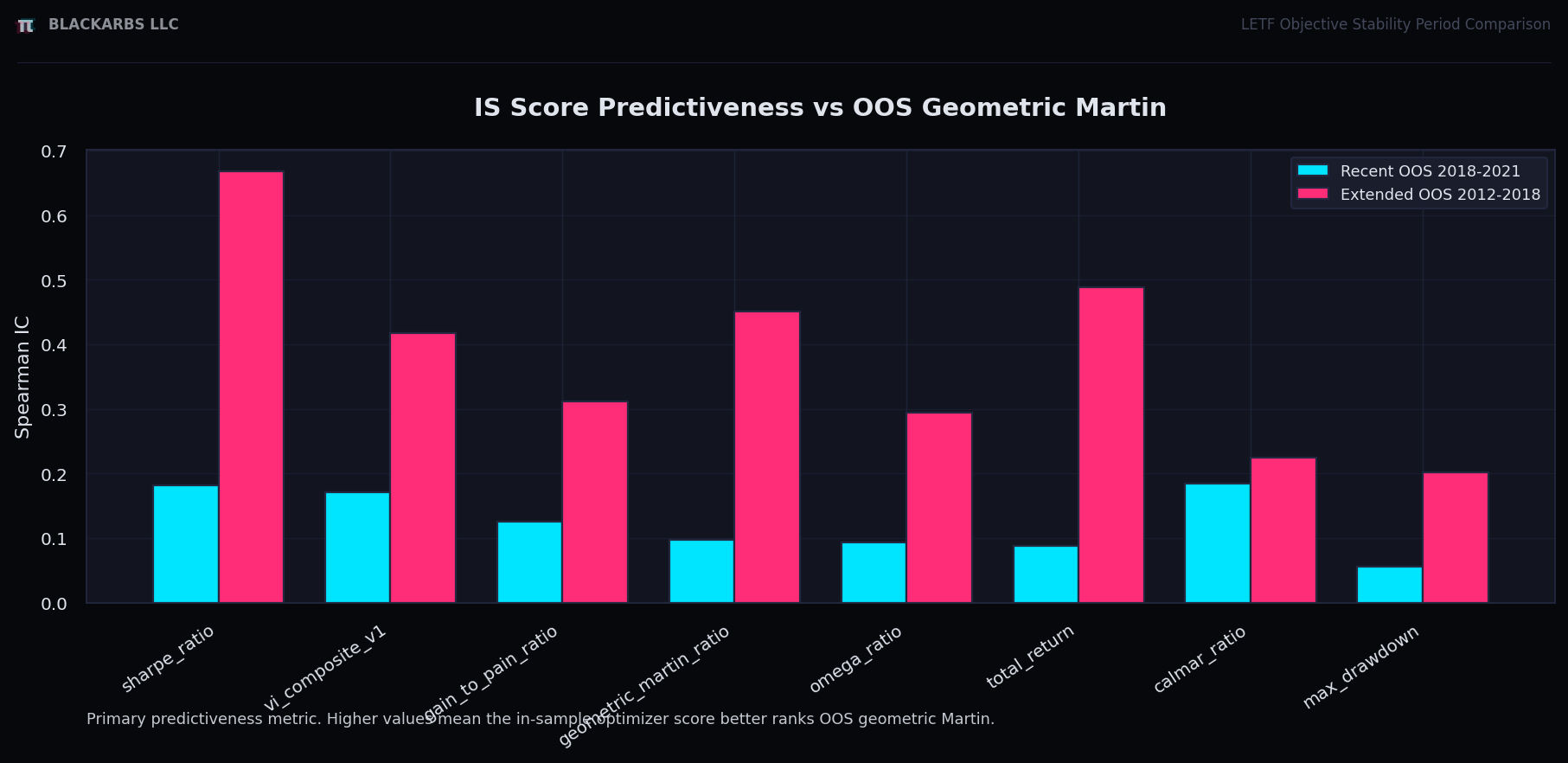

Did the optimizer score predict better future paths?

This asks whether higher in-sample optimizer scores actually pointed to better future path quality.

The longer future test made the signal clearer.

A target can look okay recently and much more decisive over a longer future period.

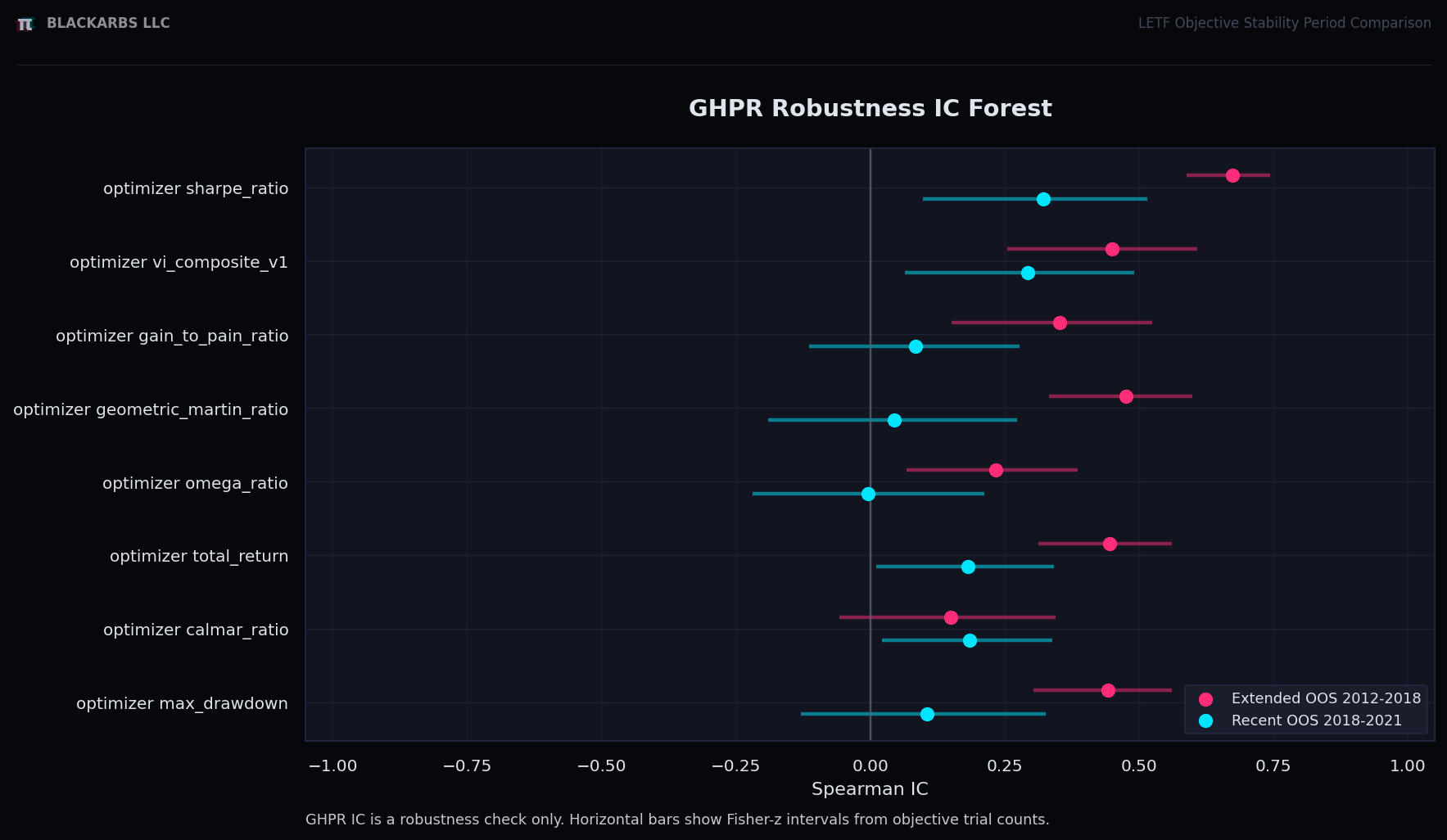

Did the result still make sense on pure growth?

This checks whether the same optimizer scores also line up with future growth.

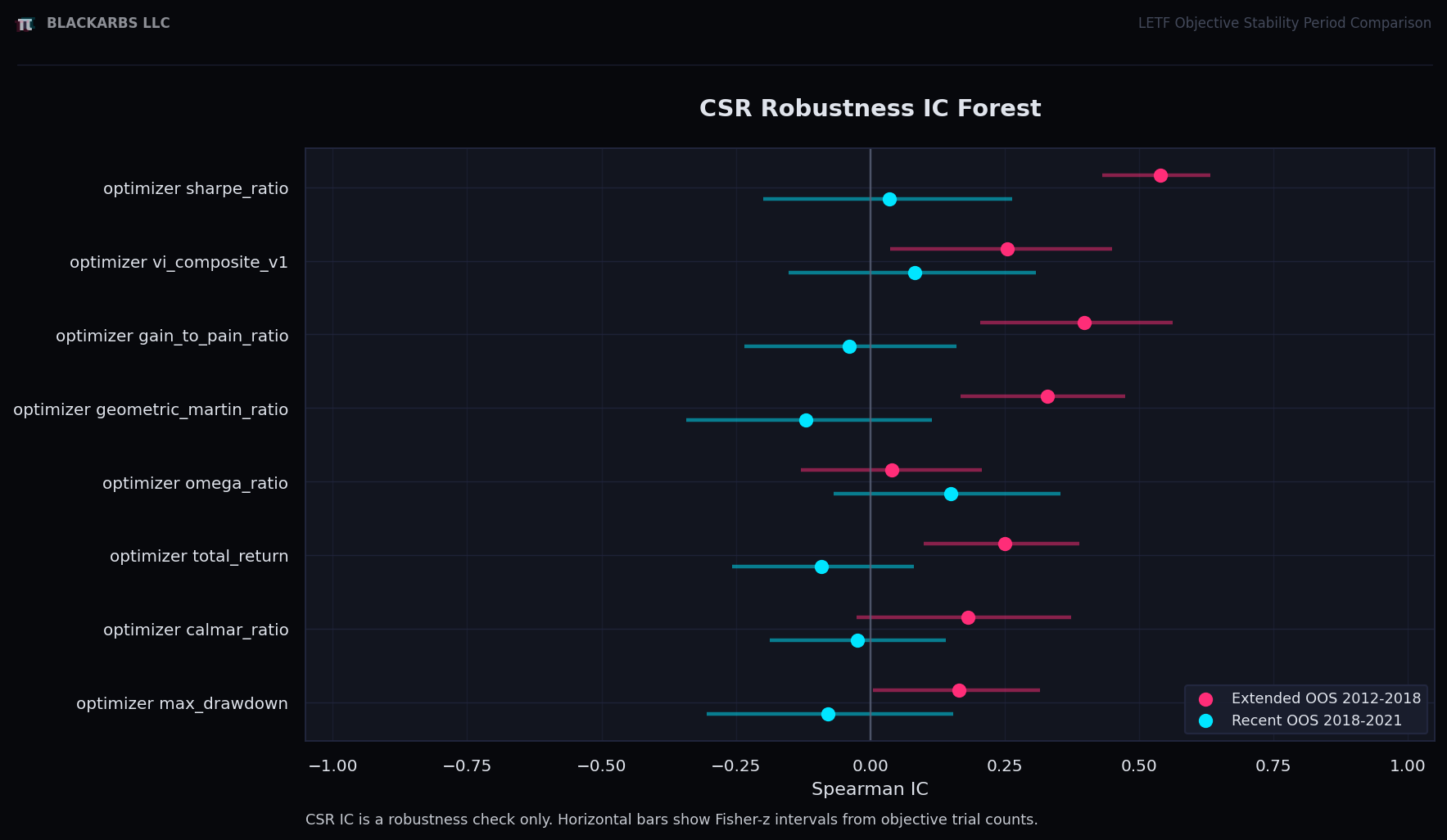

Did the result still make sense after looking at bad tails?

This checks whether the optimizer score also lines up with cleaner upside/downside behavior.

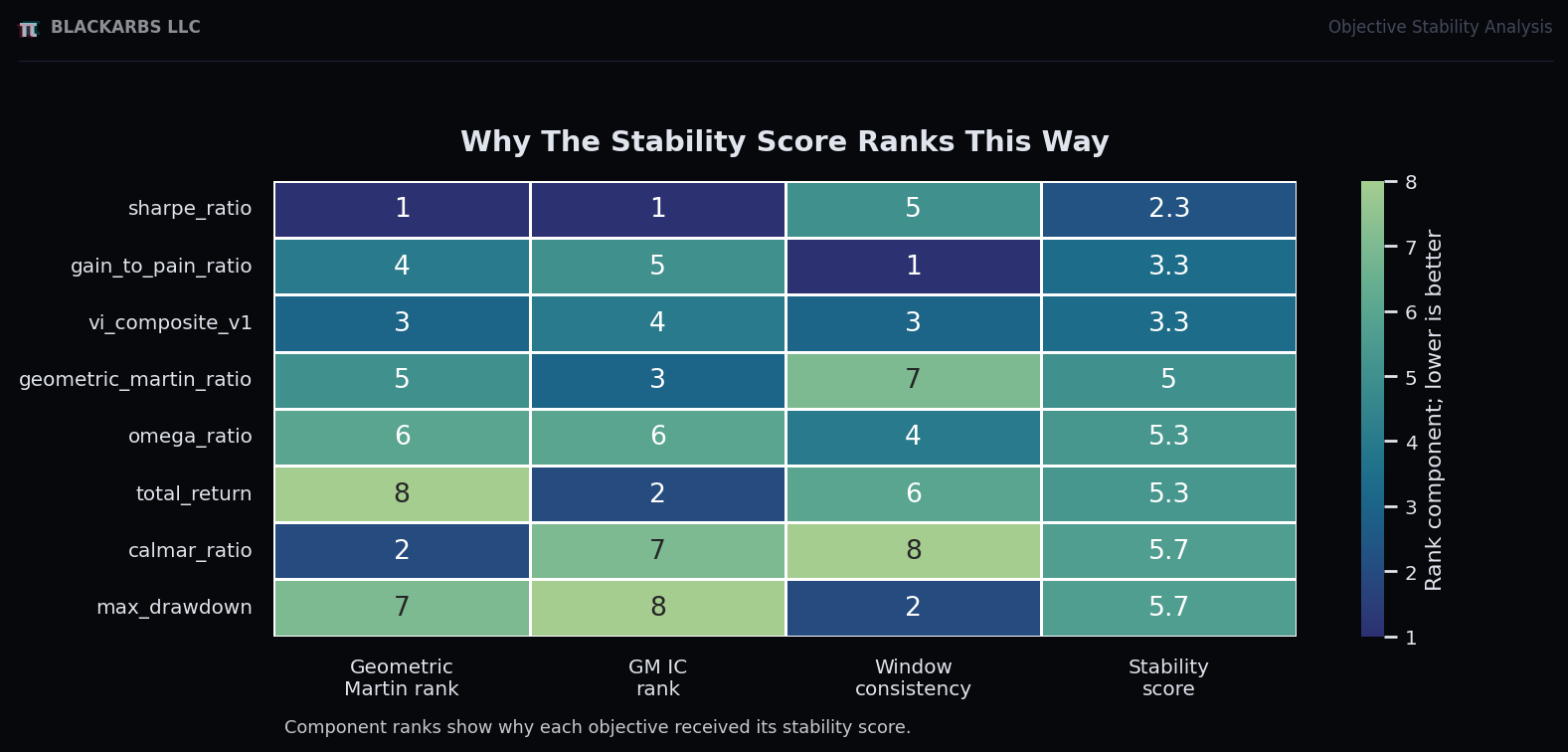

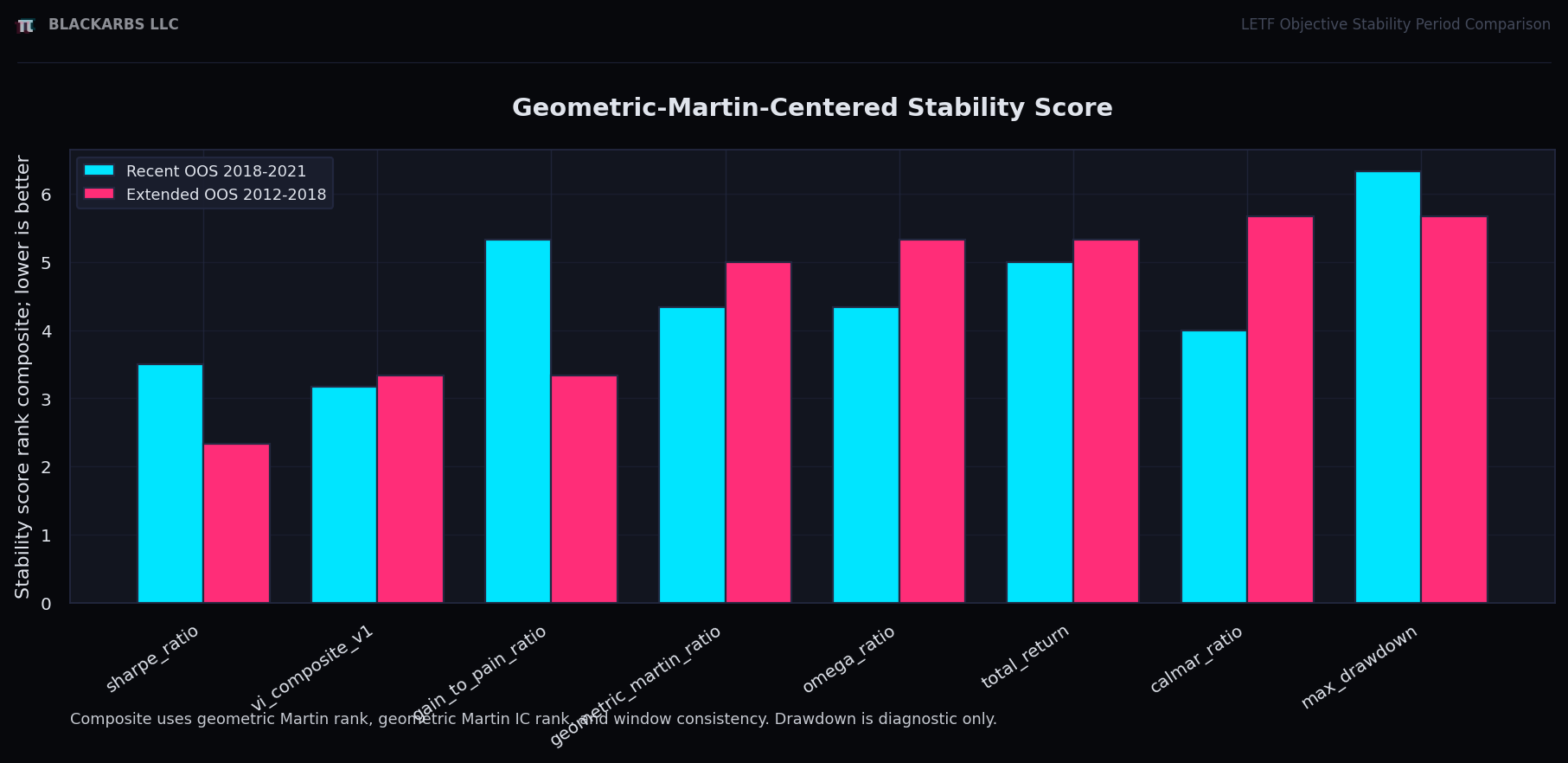

Put the evidence into one stability ranking.

The final ranking combines future path quality, predictive power, and consistency. Lower is better.

Why does the longer holdout rank them this way?

The direct geometric-Martin objective had a decent IC, but weaker longer-period path rank and consistency.